De Minimis Tax Thresholds and Cross-Border E-commerce

The approaches to De Minimis tax thresholds form a growing subject of interest within cross-border e-commerce. When an item that is purchased online passes through a customs barrier, its value is compared against the De Minimis level (Latin for ‘from the smallest’) set by the destination country’s government; usually in the form of a monetary figure. No duties or taxes are applied if an item’s value is below this level. However, if an item’s value is above this level, it is liable for additional charges. The rapid growth of e-commerce has exposed the outdated nature of many De Minimis regimes around the world, and several major markets are applying methods to adapt their taxation strategies.

Most De Minimis levels were historically set for traditional trade methods, and several existing designs now inadvertently affect e-commerce activities. However, altering De Minimis values can be a difficult and controversial decision for national governments as they try to balance advantages for local manufacturers (and jobs) against the commercial needs of citizens. Changes to De Minimis levels will inevitably disturb one of these sectors. It is the role of a government to determine whether the benefits of such changes outweigh potential domestic political or financial fallout. For online retailers, added costs due to duties and taxes can result in higher levels of shopping cart abandonment at checkout. These costs can, in-turn, reduce the attractiveness of a site to customers from certain countries, or force these customers to use grey-market or daigou agent (‘on behalf of’) options to avoid greater charges.

In 2017, GEODIS commissioned a study to review the various approaches to De Minimis levels at an international level – particularly concerning lower-value online goods – and how governments are adapting their taxation laws. We examined and compared seventeen major e-commerce markets on five continents during the course of this study. To summarize, we found that international approaches to De Minimis levels can be divided at a macro level into three broad groups – protectionist, competitive and stationary.

Protectionist

E-commerce has the potential to pose a threat to traditional domestic markets, particularly where certain products are difficult to obtain or are highly taxed locally. Cheaper international prices, multiple delivery options and greater variety of goods can result in significant expenditure directed towards foreign retailers, putting pressure on governments to defend domestic businesses and jobs.

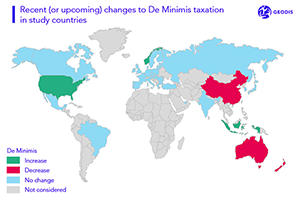

One of the few effective tools available for governments is to make cross-border online purchases less attractive through higher taxation or lowering De Minimis levels. This is the case in Canada, where the De Minimis threshold was set in the 1980s at just CAN$20, primarily to defend local industry. Though Canada’s De Minimis regime is popular with resident manufacturers, it has recently proven to be a major impasse within the NAFTA trading block and is deeply unpopular with Canadian online shoppers. A recent poll suggested that 76% of Canadians would like to see the limit raised to at least CAN$200, which would still be well below the USD$800 level in the neighboring United States.

The potential of added revenue from the heavier taxation of overseas online goods can be a primary argument for a protectionist De Minimis approach. In Q2 2017, Australia planned to reduce their De Minimis value from AU$1000 to AU$0 as a method of generating taxation from international e-commerce. However, implementation was deferred until July 2018 by the Australian Senate due to difficulties in determining how the extra taxation was to be collected. It is still an open point for discussion. In theory, a zero limit may seem attractive to governments. However, a counterpoint to this argument is that the cost of processing low value items can exceed the revenue gained, thus negating any benefit to a government’s exchequer.

Of all the protectionist approaches, China’s is complex but perhaps also the most adaptable to international e-commerce. Introduced in 2016, the law reduced the De Minimis level to CNY50 (USD$7), using a stratified import tax system that applies a yearly and per transaction De Minimis limit per user. This ensures that occasional online shoppers are not taxed as heavily as those making frequent, expensive or large volume online purchases.

Competitive

Governments who hold a competitive approach to De Minimis levels seek to open both domestic and cross-border lanes to consumers by maintaining threshold levels. For some, like Hong Kong, high or non-existent De Minimis rates have been in place for many decades and are imbedded in the national commercial psyche. In fact, they are part of a wider economic approach to attract international trade. Others, such as Indonesia or the United States, have only recently increased their De Minimis levels, hoping that greater international trade will also stimulate domestic markets.

Stationary

Stationary De Minimis tax regimes are by far the most frequently encountered and can be subdivided into two primary groups:

Mature e-commerce/tax relationship

Countries such as Japan, with a mature e-commerce/tax relationship, often recognize the impact that cross-border online trade has on their populace. Though many countries within this category maintain low De Minimis levels, they have aided international imports through simplified customs procedures or low duty rates above De Minimis. Others, like South Korea and the United Arab Emirates, assist cross-border e-commerce through expanding existing trade deals with significant e-commerce origin markets or regional/trade-block neighbors.

Immature e-commerce/tax relationship

Immature e-commerce/tax relationships stem from the unprecedented growth of online retail and the inability of governments to adapt their import tax systems accordingly. The European Union openly admits that their existing €22 De Minimis threshold is outdated, as it was established prior to the emergence of online shopping as a major economic force. Countries that have yet to adjust their tax arrangements to modern cross-border e-commerce trends may also simply be observing how recently-implemented protectionist or open market policies perform prior to implementing an appropriate tax structure.

During the coming years, the issue of De Minimis limits for cross-border e-commerce will become a more prevalent discussion point for national governments, logistics providers and online retailers. Changes in existing De Minimis levels, both in emerging and maturing e-commerce markets, can be expected and should be reviewed at regular intervals as part of basic policy by logistics providers.

by

by

by

by

by

by