JUNE 2022 GEODIS INDUSTRY UPDATE

19/07/2022

19/07/2022Welcome to the June 2022 GEODIS Industry Update digest

Our monthly Industry Update provides the latest nationwide economic data, fuel-related concerns, modal rate outlooks, indexes as well as a variety of additional statistics and news items to provide a broad overview of what’s impacting the U.S. transportation industry nationally and globally.

Economic Overview

GDP

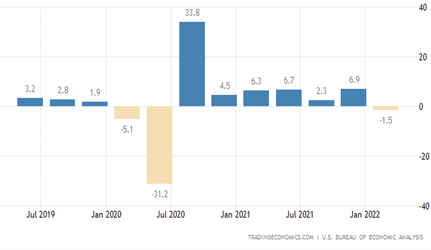

The U.S. economy contracted an annualized 1.5% on quarter in the first three months of 2022, slightly worse than initial estimates of a 1.4% decline, with the biggest drag coming from trade. Imports surged more than initially anticipated (18.3% vs 17.7% in the advance estimate), led by nonfood and nonautomotive consumer goods and exports dropped slightly less (-5.4% vs -5.9%), mainly due to nondurable goods. Consumer spending though rose more (3.1% vs 2.7%), led by housing and utilities and motor vehicles and parts while spending on gasoline and other energy goods decreased.

U.S. Trade Deficit (June 2022)

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis has announced that the goods and services deficit was $87.1 billion in April, down $20.6 billion from $107.7 billion in March, revised. April exports were $252.6 billion, $8.5 billion more than March exports. April imports were $339.7 billion, $12.1 billion less than March imports. The April decrease in the goods and services deficit reflected a decrease in the goods deficit of $19.1 billion to $107.7 billion and an increase in the services surplus of $1.5 billion to $20.7 billion.

Unemployment Rate

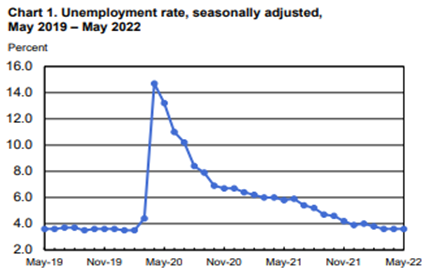

The U.S Bureau of Labor Statistics reports that nonfarm payroll employment increased by 390,000 in May and the unemployment rate remained at 3.6 percent. Notable job gains occurred in leisure and hospitality, in professional and business services, and in transportation and warehousing. Employment in retail trade declined.

Labor Participation Rate

The labor force participation rate in the U.S. edged up to 62.3 percent in May of 2022 from a 3-month low of 62.2 percent in April. The share of the population that is working or looking for work remains 1.1 percentage points below their February 2020 values, as Americans that left work during the pandemic are coming back slowly due in part due to childcare and early retirement.

Manufacturing

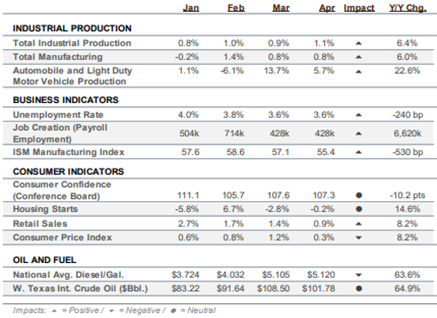

The ISM manufacturing index improved by 0.7 percentage point to 56.1 in May, indicating a slight overall acceleration in the sector. The new orders and production components strengthened and inventory growth was the strongest positive, but customers’ inventories were reported as too low.

Consumer

Retail sales increased 0.9% in April, following an upwardly revised 1.4% advance in March. Inflation contributed to the gain, but sales rose in real terms as well. Rising wages and significant savings support continued spending despite headwinds. Gasoline sales fell 2.7% in April, but they will rise in May’s data. Excluding gasoline and the auto sector, sales advanced 1.0% in April.

Residential Construction

New residential investment softened modestly in April, but a sharp decline in permits may be pointing to a cooler future. Housing starts slipped 0.2% to 1.724 million units. Single-family starts fell 7.3% while the multi-family sector saw starts jump 16.8%. Total permits fell 3.2% to 1.819 million. The decrease was in the single-family sector. Mortgage rates are above 5%, and applications for mortgages are down 15% from a year earlier, suggesting weaker activity.

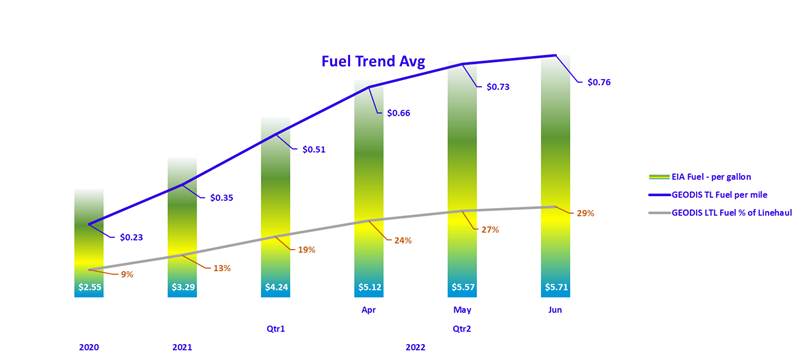

Fuel Forecasts and Trends

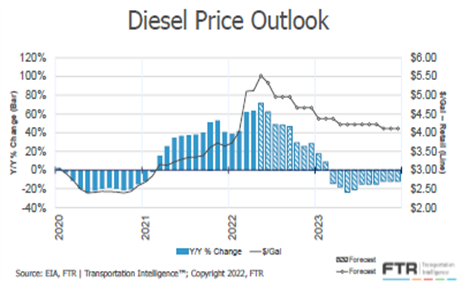

After stabilizing at near-record levels in April, diesel prices soared again in May and in early June. The national average price on June 6 was a record $5.703 a gallon. One culprit appears to be low distillate stocks, especially on the East Coast. Meanwhile, crude prices continue to move higher and have been trading at around $118 a barrel recently.

The Brent crude oil spot price averaged $113 per barrel (b) in May. We expect the Brent price will average $108/b in the second half of 2022 (2H22) and then fall to $97/b in 2023. Current oil inventory levels are low, which amplifies the potential for oil price volatility. Actual price outcomes will largely depend on the degree to which existing sanctions imposed on Russia, any potential future sanctions, and independent corporate actions affect Russia’s oil production or the sale of Russia’s oil in the global market.

The U.S. average retail price for regular grade gasoline averaged $4.44 per gallon (gal) in May, and the average retail diesel price was $5.57/gal. Rising prices for gasoline and diesel reflect refining margins for those products that are at or near record highs amid low inventory levels. We expect the gasoline wholesale margins (the difference between the wholesale gasoline price and Brent crude oil price) to fall from $1.17/gal in May to average 81 cents/gal in 3Q22, and we expect retail gasoline prices to average $4.27/gal in 3Q22. Diesel wholesale margins in the forecast fall from $1.53/gal in May to $1.07/gal in 3Q22, and retail diesel averages $4.78/gal in 3Q22.

As fuel has continued to rise, the expense has become a larger percentage of the total cost of the shipment. Fuel has more than doubled throughout the country and analysts predict the

prices to remain elevated for months to come. Fuel has the potential to be 25%+ of the cost of the shipment if fuel hits $7.

Modal Update

Logistics News Flash:

Diesel once again racing higher than prices for crude oil, gasoline

Diesel prices have wrapped up four days of trading in which they are finishing far higher than they were at the start of the business week and have moved up faster than crude and gasoline prices.

It’s a worrisome trend for consumers because it signals that once again, diesel is moving at a pace more bullish than that of the petroleum market as a whole. That it already has done so in recent months is evident in the gasoline-diesel spread seen on price signs outside of retail outlets, and it has a complex set of causes.

Ultra low sulfur diesel for July delivery settled on the CME commodity exchange Friday at $4.2803 a gallon. That marked a gain of 7.19 cents per gallon on the day for an increase of 1.71%. It traded as high as $4.3250.

For the week — which was just four trading days, given the Memorial Day holiday — July ULSD rose 9.6%, posting a gain of 37.5 cents per gallon.

By contrast, the gain in WTI over the four days (from the May 27 settlement through the settlement at the end of this week) was 3.3% for West Texas Intermediate crude, barely any overall movement for global crude benchmark Brent, and 8.6% for RBOB, an unfinished gasoline blend stock that is a trading proxy for gasoline.

Those sorts of numbers suggest that increasingly, the issue in the market is not just the loss of Russian crude supplies but a loss of refining capacity worldwide that is coming home to roost, aggravated by the effective loss of some Russian refining capacity and its output as a result of formal and informal sanctions.

It is most evident in one of the most basic numbers traders watch: the 3:2:1. It’s a rough estimate of refining margins, arrived at by taking the price of either Brent or WTI and multiplying it by 3, and then subtracting that number from the sum of taking two barrels of gasoline and one barrel of ULSD.

The 3:2:1 for both Brent and WTI spent most of the week in the range of $55 to $60 per barrel, depending on how it was calculated. (Even a simple number like this can be the focus of differences in methodology.) At the start of 2021, it was closer to $20 a barrel, a figure that was far more in line with historic norms. A 3:2:1 in the upper $50s is leaving traders searching for new words to describe how unprecedented that is.

That sort of blowout can be expected in a world in which the International Energy Agency estimated earlier this year that global refining capacity had a net decline of 730,000 barrels per day in 2021. While that is less than 1% of the global oil market, in a tight supply/demand balance, the impact of such a decline can be enormous.

Source for full article: https://www.freightwaves.com/news/diesel-once-again-racing-higher-than-prices-for-crude-oil-gasoline

Diesel is used in the U.S. mostly in trucks, which means higher prices add to shipping and delivery costs. Inventories of distillates, which also include heating oil, fell recently to a 17-year low in the midst of lower refining activity and higher demand domestically and abroad, according to the U.S. Energy Information Administration. Supplies are particularly tight along the East Coast, where inventories have dropped to their lowest level since at least 1990.

In Europe, where diesel cars account for a bigger chunk of the auto fleet, prices in the wholesale market have leapt 88% over the past year. The availability of fuel is likely to worsen as sanctions on Russia tighten, exposing a flaw in the region’s energy setup.

Governments in recent decades pushed drivers to adopt diesel cars but didn’t upgrade the refinery industry so it could produce the fuel in greater quantities. That meant buying more diesel from Russia, the energy superstore on Europe’s doorstep.

Helge Ippendorf, chief executive of Via Logistik GmbH, a company based near the German city of Cologne that trucks artwork, road-safety materials and other wares, is shelling out 4,000 euros, the equivalent of $4,150, a week for diesel, 80% more than a year ago. He can’t remember such a jump in fuel prices since the 1970s oil shocks.

“No other impact in my whole career—and I started my own company in 1981—was as massive as the situation at the moment,” he said.

Rising energy prices are a major factor contributing to the persistence of inflation, which has sparked steep declines in the stock and bond markets. The S&P 500 fell 1.6% Wednesday after a gauge of U.S. consumer prices came in higher than Wall Street expected.

Source for full article: https://www.wsj.com/articles/record-diesel-prices-pressure-european-drivers-u-s-deliveries-11652416873?mod=djemlogistics_h

Railroad, Union Labor Fight Moves Toward Biden Intervention

Major railroads, including Union Pacific Corp. and BNSF Railway Co., and their unions remain at an impasse after a government board ended efforts to mediate a settlement, a move which will likely force President Joe Biden’s administration to intervene and prevent a strike that could cripple an already-strained U.S. supply chain.

The National Mediation Board sought to move the negotiation into binding arbitration, but the union has rejected that offer, the National Carriers’ Conference Committee said in a statement on its website. The talks will now enter a 30-day cooling off period and then a presidential emergency board appointed by the White House resolve the dispute.

“The railroads would consider accepting the proffer, but the union leadership has already indicated that it will not,” said the committee, which also represents CSX Corp., Norfolk Southern Corp. and Kansas City Southern, which is being acquired by Canadian Pacific Railway Ltd. “The railroads expect a PEB will be appointed in this dispute before the end of the 30-day cooling off period, as has been the case in prior unresolved national rail negotiations,” it said in the statement.

A rail strike would severely constrict the supply of goods across the country, which is still recovering from bottlenecks caused by the pandemic. If the presidential board can’t resolve the issues, then Congress would have to step in. If federal legislators fail, then the union could call a strike or the railroads could hold a lockout.

The White House did not immediately comment.

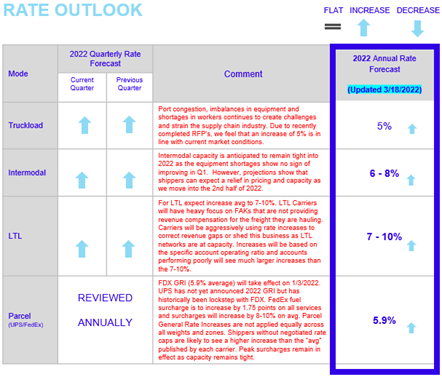

The outlook for LTL rates is a 6.2% increase y/y, up from 5.8% previously. The 2023 forecast is a 5.6% decrease.

The truckload rate outlook is slightly weaker than in the prior forecast at a 3.8% y/y increase, down from 4.5%. The forecast for 2023 is a 3.4% y/y decrease in rates. Spot rates in 2022 are forecast to be down about 2% y/y, which is sharper than in the previous outlook. The projected 7.5% increase for contract rates is marginally weaker than in the prior forecast.

Intermodal rate expectations were little changed in the latest month with a declining trend expected through the end of the year. While last year’s gains will not recur, growth will hold at present levels, approaching flat by the end of the year.

The talks, which involve about 115,000 union rail workers and more than 30 railroads, began in January 2020. The unions have said the two sides are far apart on issues such as work rules and benefits, and complained their workers are stuck under the contract frozen since 2019.

“Our members are the essential workers who keep the supply chain moving safely every day,” said Dennis Pierce, national president of the Brotherhood of Locomotive Engineers and Trainmen, one of the unions participating in the talks. “Despite record profit by the Class I railroads, our people have failed to get an extra dime in contract raises during the pandemic and struggled to get any time off.”

The unions said they rejected arbitration because their rank-and-file membership can’t vote on any binding solution resulting from such a process. With a presidential board, union members can vote to approve or turn down a proposed deal.

Source for full article: https://www.bloomberg.com/news/articles/2022-06-14/railroad-union-labor-dispute-moves-closer-to-biden-intervention

Logistics Hiring Slowed in May Amid Shifts in Retail Sector

Companies on the front lines of supply chains pulled back hiring in May amid signs that the boom in e-commerce demand is waning and consumers are shifting spending from goods to services. Trucking, warehousing and parcel-delivery companies added a combined 32,900 jobs last month, according to seasonally adjusted preliminary employment figures from the U.S. Bureau of Labor Statistics, down from 44,700 jobs added in April.

The pullback came as the broader U.S. economy added 390,000 jobs in May, in the slowest pace of growth in more than a year but still far above employment expansion before the pandemic. The expansion in the trucking and warehousing sectors suggests logistics operators are continuing to staff up in a tight labor market as they work to unscramble supply chains.

Trucking companies added 13,300 jobs last month and have boosted employment by more than 70,000 jobs over the past year as operators have tried to keep up with strong freight demand. The figures suggest trucking companies are having success in recruiting efforts that have included higher starting salaries and sign-on bonuses, said Cathy Roberson, president of research and consulting firm Logistics Trends & Insights LLC.

“I think we are seeing some independent [owner-operator truck drivers] taking jobs with the larger trucking companies,” Ms. Roberson said.

Parts shortages and production delays still appear to be hindering further growth. FTR Transportation Intelligence said Friday that preliminary North American orders for Class 8 heavy-duty trucks fell to 13,300 big rigs in May, down 43% from the same month last year and the lowest level for orders since November 2021.

Source for full article: https://www.wsj.com/articles/logistics-hiring-slowed-in-may-amid-shifts-in-retail-sector-11654276598?mod=djemlogistics_h

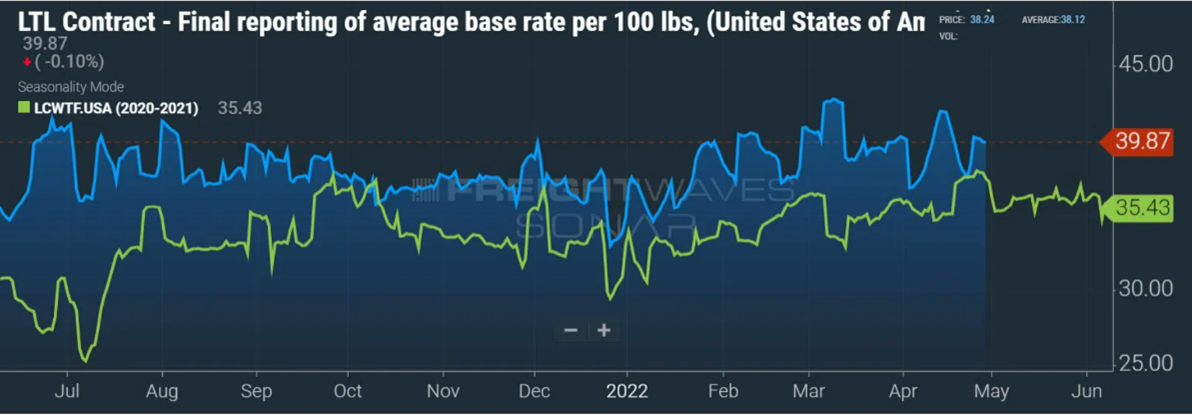

Rate Outlook Updates: Contract LTL, Truckload and Intermodal

LTL contract rates look significantly stronger for 2022 in the latest forecast with a projected 9.8% gain y/y.

The truckload rate outlook continues to soften with total rates forecast at +3.5% y/y in 2022, excluding fuel, down from +3.8%. However, a larger forecasted gain in contract rates mostly offsets a larger drop in spot. The forecast for 2023 is a decline of 3.2% in total rates.

The trajectory of intermodal rate increases is little changed this month with a slow erosion of pricing power expected. Rate increases are expected to decline to near flat by the end of the year, but that means carriers are not giving back any of the gains they established last year.

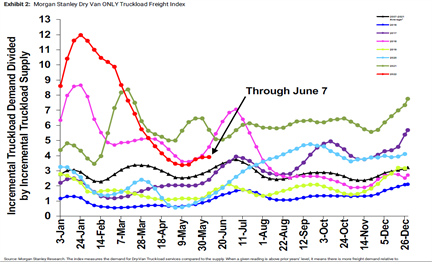

Morgan Stanley Index

Demand and supply both underperformed and contributed to the index level result as the underlying components missed typical seasonal trends by ~1,200 and ~470 bps respectively. Sequentially, the demand component increased by ~170 bps while the supply component decreased by ~180 bps driving the overall index to move higher (but less than expected for this time of year). Our Flatbed index and Reefer index both also underperformed seasonality and flipped from “green” to “red” in addition to declining sequentially. This is not necessarily surprising as we previously noted that last update’s performance may have benefited from Road check in May, which has historically created additional tightness in the market.

Cass TL Linehaul Index (June 2022)

The shipments component of the Cass Freight Index® rose 5.4% m/m in May (up 4.0% SA), more than recovering the 2.6% decline in April. On a tough comparison, the y/y decline worsened to 2.7%, as expected, but the result was 1% ahead of the ACT Research estimate. Normal seasonality from here would have the shipments component back up 2% y/y in June and flat to up 1% for 2022. The news from the retail sector and in the oil, markets suggest that’s probably optimistic, but at this point, it’s a pretty stable environment. No major downturn. The expenditures component of the Cass Freight Index, which measures the total amount spent on freight, fell 4.9% m/m in May with shipments up 5.4% and rates down 9.8%.

Parcel Update:

Is FedEx charting different course with board, incentive plan changes?

Less than two weeks into the tenure of new CEO Raj Subramanian, FedEx Corp. appears to be charting a new path.

FedEx (NYSE: FDX) has announced an array of changes that included the appointment of three new directors, a revised executive incentive plan and a 53% increase in the company’s quarterly dividend to $1.15 a share.

More light will be shed on the significance of the moves at FedEx’s analyst and investor meeting June 28 and 29 in the company’s hometown of Memphis, Tennessee. However, the actions appear to telegraph a change in management’s priorities under Subramaniam, who became CEO on June 1.

V. James Vena, who served as chief operating officer at Union Pacific Corp. (NYSE: UNP) and Canadian National Inc. (NYSE: CNI), and Amy B. Lane, who sits on the board of retailer TJX Companies Inc. (NYSE: TJX), will join FedEx’s board as part of an agreement with D.E. Shaw Group, a shareholder activist organization and a large FedEx shareholder. A third director, who will be a mutual choice of FedEx and Shaw, will join the board at a later date.

The board announcements may signal a new level of cooperation between FedEx and outside shareholders, which had been limited in part by the powerful specter of Frederick W. Smith, FedEx’s founder, former CEO and largest individual shareholder. Smith became executive chairman June 1 to make way for Subramaniam’s ascension to the CEO role.

As part of changes to the management long-term incentive plan over the next three fiscal years — fiscal 2023 began June 1 — FedEx will tie cash incentives to a ratio of capital expenditures to revenue. The target ratio will reflect what is expected to be lower capital expenditures over the next three fiscal years compared to prior years, FedEx said. The company had projected $7.2 billion in capital expenditures during fiscal 2022.

Source for full article: https://www.freightwaves.com/news/is-fedex-charting-different-course-with-board-incentive-plan-changes

Current LTL Market:

Yellow’s Q2 volumes fall again amid network overhaul

Volume declines continued for less-than-truckload carrier Yellow Corp. in May. The company reported a 17.2% year-over-year decline in tonnage during the month, which followed a similar drop in April. The declines are part of a plan to cull unwanted freight from the network and drive yields and margins higher.

On Yellow’s (NASDAQ: YELL) first-quarter earnings call, management said the tonnage declines had peaked in February, which saw a 27% year-over-year drop. March was down 18% and a preliminary assessment of April called for a decline of 14% to 15%. April ultimately came in worse than expected, but it appears that the freight drops have stabilized, albeit at still sizable declines.

“The quarter-to-date operating metrics for the second quarter are consistent with our expectations as we work to ensure the optimal level of freight is moving through the network,” said CEO Darren Hawkins in a press release. “With continued steady demand for LTL capacity and a consistent favorable pricing environment, our financial results for the first two months of the quarter have outperformed our historical sequential improvement from Q1.”

The company is consolidating and closing terminals in its Western network, with two additional phases planned by the end of the year. Yellow has already consolidated its four LTL operating companies and its logistics unit under the same roof.

So far in the second quarter, shipments have fallen 15.3% compared to the year-ago period and weight per shipment is off by 2.2%. However, revenue per hundredweight, or yield, is up nearly 30%. Higher fuel surcharges — up 70% year-over-year so far in the second quarter and 27% higher on average than in the first quarter — have provided a big tailwind to yields.

“Our plan is to grow the business and we are confident that our transformation to One Yellow positions us for long-term tonnage growth,” Hawkins continued. “We expect the One Yellow network transformation to enhance customer service, lead to greater efficiencies and cost savings and add capacity to the network.”

Source for full article: https://www.freightwaves.com/news/yellows-q2-volumes-fall-again-amid-network-overhaul

Current Truckload Market:

Heartland acquires dry van truckload carrier Smith Transport

Heartland Express has returned to the acquisition market with the purchase of a dry van truckload company, Smith Transport.

In its first acquisition since it bought Mills Transfer in August 2019, Heartland paid approximately $170 million for all the equity in Smith and related companies.

“During the pandemic, it was a barren wasteland for mergers and acquisitions,” Heartland Chairman, President and CEO Michael Gerdin said.

Gerdin said M&A activity began to pick up at the end of 2021 and that is when Heartland began discussions with Pennsylvania-based Smith Transport.

“We wanted somebody with decent size,” he said. “These guys put up $200 million in gross revenue last year.”

The acquisition price is slightly below the $187 million in cash that Heartland (NASDAQ: HTLD) had on its books at the end of the first quarter. In its prepared statement, Heartland said the acquisition was funded with existing cash.

But in the telephone call with FreightWaves, Gerdin and CFO Chris Strain said the cash outlay from Heartland was about $155 million, with the $170 million enterprise value put on Smith Transport being a function of both debt and cash Smith held as well as a separate real estate transaction valued at $14 million. .

Additionally, the cash position of Heartland at the end of the first quarter has changed significantly, in part because of a sale announced last week of a California terminal the company owned in the Inland Empire.

Heartland, in a Securities and Exchange Commission filing on the sale, said it netted a pretax gain on the sale of about $73 million. A gain of that size would be close to all of the company’s net income for 2021, which came in at $79.3 million.

Source for full article: https://www.freightwaves.com/news/heartland-acquires-dry-van-truckload-carrier-smith-transport

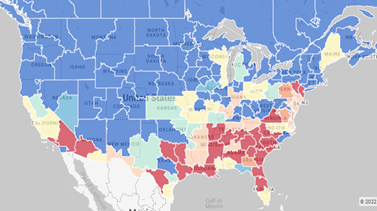

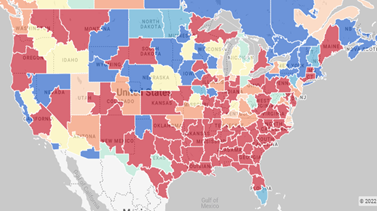

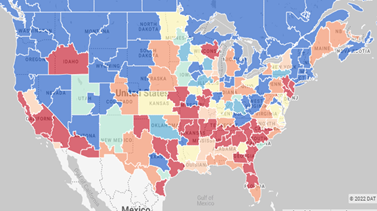

DAT Hot States: Vans, Flatbeds and Reefers

DAT Hot States for vans, flatbeds and reefers uses the MCI cool to hot, or -100 to +100, scale for measuring market temperature.

On the following U.S. maps, when the market is cool (darker blue areas), capacity is loose and in the negative range. When the market is hot (darker red areas), capacity is tight and in the positive range. The lighter colored areas (including yellow) capacity is more neutral.

Vans – June 2022

Flatbeds – June 2022

Reefers – April 2022

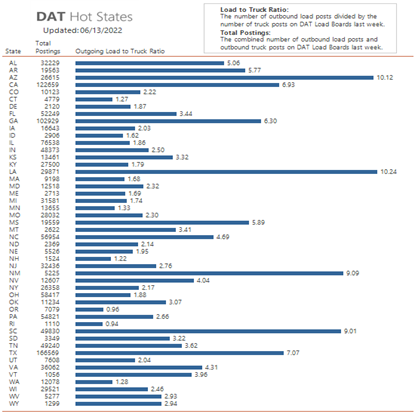

The load to truck ratio from DAT is a strong indicator of the balance between demand and capacity. Changes in the ratio could mean changes in rates. The higher the ratio, the tighter the capacity is for a particular state. As of June 13, 2022, DAT Hot States, the state with the highest load to truck ratio was Louisiana (10.24) with Rhode Island (0.94) the lowest for the month.

Rate Outlook, Regulatory Update and Closing Thoughts

Food Prices to Keep Going Up, as Costs Surge

Some of the nation’s biggest food suppliers and restaurants, including Kraft Heinz Co. and some McDonald’s Corp. franchisees, said they would continue to raise prices as they face starkly higher costs.

Kraft Heinz has notified retailer customers that it would raise prices in August on items ranging from Miracle Whip and Classico pasta sauce to Maxwell House coffee products and some deli meat. Cory Onell, chief sales officer at Kraft Heinz, wrote in the memo to retailers that inflation continues to affect the economy and shape consumption patterns. Costs continue to rally, and the persistence of increases makes it necessary to announce price changes, he wrote.

From farmers and factories to grocery stores and restaurants, many executives say they are experiencing jaw-dropping cost increases for labor, packaging, ingredients and transportation. The rise of fuel prices is making it more expensive to produce and sell food. Food retailers and restaurants have said they are passing along some wholesale price increases and additional costs to consumers.

The Labor Department said grocery prices rose 11.9% in May over the past year, and prices increased 7.4% at restaurants and other food venues outside the home in the period. For both, it marks the biggest jump in over four decades.

Russia’s invasion of Ukraine, one of the world’s top grain-producing regions, is lifting the price of pantry staples, cooking oils and livestock feed for meat. Bad weather affecting other big crop-producing countries, including in parts of South America, Australia and India, is fueling the global crunch, too.

Kraft, commenting on the coming price increases, said they reflect the costs of production the entire industry is facing.

Many food makers, including Kraft, have already raised prices this year. Kraft has raised prices 13.9% since 2019, Chief Executive Officer Miguel Patricio said at an investor conference earlier this month. He said other brands have followed, and because price increases are widespread across stores, consumers aren’t reacting as much as they have historically.

Still, in recent months, more people have switched to buying less expensive brands or cuts of meat at grocery stores and eating out at restaurants less often, industry executives said, as inflation and gas prices weigh on household budgets.

Companies are finding other ways to offset inflation, too. They sell smaller packages for a higher price per ounce. And they make operations more efficient to save money. Kraft, for example, said it is improving its productivity at factories. “If we only rely on price increases, we’re going to have problems,” Mr. Patricio said.

To soften the blow of price increases, food makers also provide deals. Kraft said it is offering some larger package sizes for a better value.

Source for full article: https://www.wsj.com/articles/food-prices-to-keep-going-up-as-costs-surge-11654939800?mod=djemlogistics_h

Transportation capacity up again in May; prices still climbing

Transportation capacity expanded for a second straight month in May after falling for nearly two years, according to a monthly survey. Overall activity in the supply chain remained firm during the month.

The Logistics Managers’ Index (LMI), a measure of overall supply chain conditions, dipped 2.5 percentage points from April to 67.1 in May. A reading above 50 indicates expansion while a reading below 50 indicates contraction.

The transportation capacity subindex jumped 7.8 points to 64.7. That was the sharpest rate of expansion in the data since October 2019, “as the logistics industry continues its regression towards the mean after nearly two years of rapid growth,” the report read.

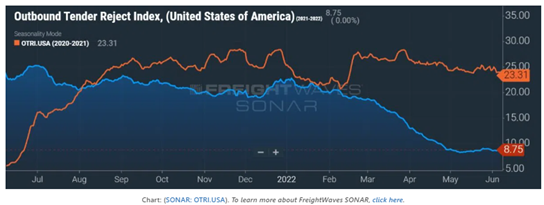

The index is now 20.3 points higher than the February reading. The change is evident in FreightWaves’ Outbound Tender Reject Index. Loads being rejected by carriers have fallen to just 9% compared to readings north of 20% throughout 2021.

The capacity situation, however, has been bifurcated by carrier size. Small carriers dependent on load boards for freight have seen fundamentals tank as lower spot rates have been met by rising costs, notably fuel. Conversely, large fleets are still seeing contractual rate increases and many management teams say they could use additional drivers and equipment.

Transportation utilization was flat at 64.3 during the month but the rate of growth in the pricing index slowed, down 8.6 points from April to 65.3. This was the slowest rate of growth in the prices data set since June 2020. However, the trend for rates is unlikely to turn negative as survey respondents indicated a value of 68.4 in a year from now.

“Despite this slowdown, it should be noted that we are still observing a healthy rate of growth in transportation, but one that pales in comparison to the unsustainable growth rates observed in 2021,” the report stated.

Additionally, the second half of May heated up. The pricing index was 16.1 points higher in the last 15 days of the month. Capacity growth slowed and utilization ticked higher.

Source for full article: https://www.freightwaves.com/news/transportation-capacity-up-again-in-may-prices-still-climbing

Closing Thoughts

Economy

With interest rates fuel prices and many other prices rising, consumers are having to brace for an impending recession. As fuel prices continue to climb, many small carriers and owner operators will likely stop driving, or merge with a larger company. This will make capacity in some markets tighten back up again. Another impact we are monitoring closely is the impending reopening of the Chinese ports. Pandemic times showed what can happen when a large amount of cargo ships flood the ports. So many ports, carriers and customers should start thinking about how best to manage this potential influx of freight.

Demand/Supply

As increasing cost of living and fuel prices continue, the demand for many retails sales have diminished. This is starting to worry many big retailers. These retailers successfully navigated heavy supply chain issues to now be faced with large amounts of inventory. This is due to the consumer spending flip from more relaxed spending habits to a more cautious mindset. With Chinese ports opening back up, they fear that more issues will follow if something is not done to stabilize the post-pandemic world.

We hope you enjoyed the latest GEODIS Industry Update digest and found it useful and informative. Please subscribe to receive future Industry Updates each month.

by

by