APRIL 2022 GEODIS INDUSTRY UPDATE

05/05/2022

05/05/2022Welcome to the April 2022 GEODIS Industry Update digest

Our monthly Industry Update provides the latest nationwide economic data, fuel-related concerns, modal rate outlooks, indexes as well as a variety of additional statistics and news items to provide a broad overview of what’s impacting the U.S. transportation industry nationally and globally.

Economic Overview

GDP

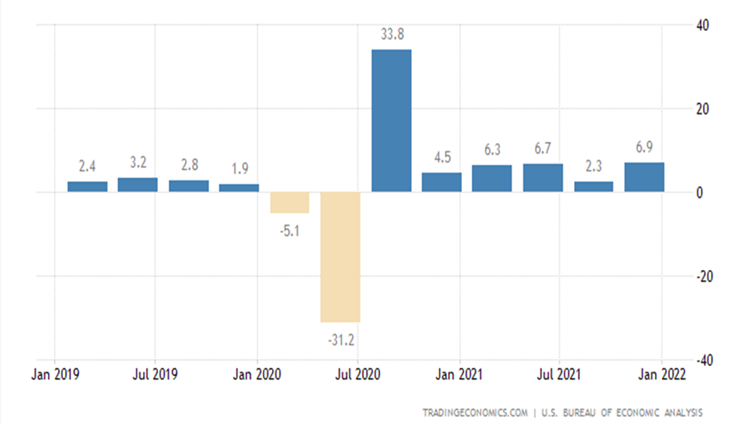

The American economy expanded an annualized 6.9% on quarter in the last three months of 2021, 0.1 percentage point lower than in the second estimate. Still, it remains the strongest expansion since a record growth of 33.8% in Q3 2020, with private inventories making the biggest upward contribution (5.32 percentage points vs 4.9 percentage points in the second estimate), led by motor vehicle dealers and wholesale trade industries.

U.S. Trade Deficit (April 2022)

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis reports that the goods and services deficit was $89.2 billion in February, down less than $0.1 billion from $89.2 billion in January, revised. The average goods and services deficit increased $3.0 billion to $86.8 billion for the three months ending in February.

Unemployment Rate

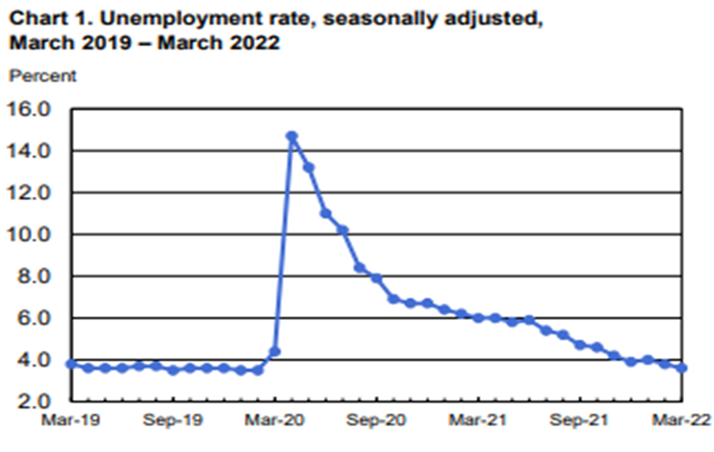

According to the U.S Bureau of Labor Statistics, nonfarm payroll employment rose by 431,000 in March, and the unemployment rate declined to 3.6 percent. Notable job gains continued in leisure and hospitality, professional and business services, retail trade, and manufacturing.

Labor Participation Rate

The labor force participation rate in the U.S. edged up to 62.4 percent in March 2022, the highest level since March 2020.

Manufacturing

The ISM manufacturing index fell 1.5 points to 57.1 in March. Although that reading keeps the sector in solid expansion mode overall, the key new orders and production components were rather weak. New orders fell 7.9 points, which was the largest negative movement in the March index. Production declined 4.0 points.

Consumer

Retail sales ticked up 0.3% in February as more expensive gasoline and food mean cuts in spending on more discretionary goods. January’s gain was revised upward to 4.9%. Most items in the retail sales data are not adjusted for inflation, so pricing boosted February sales. Sales at gasoline stations shot up 5.3% in February, but gas prices jumped 24 cents in that month.

Residential Construction

New residential construction rose sharply in February as the drag from cold weather eased. Total housing starts jumped 6.8% to an annual pace of 1.769 million. Single family starts increased 5.7%. The multi-family sector rose 0.8%. Permits fell 1.9%. Demand remains strong, but headwinds are growing. Building materials prices are high, and labor is tight.

Fuel Forecasts and Trends

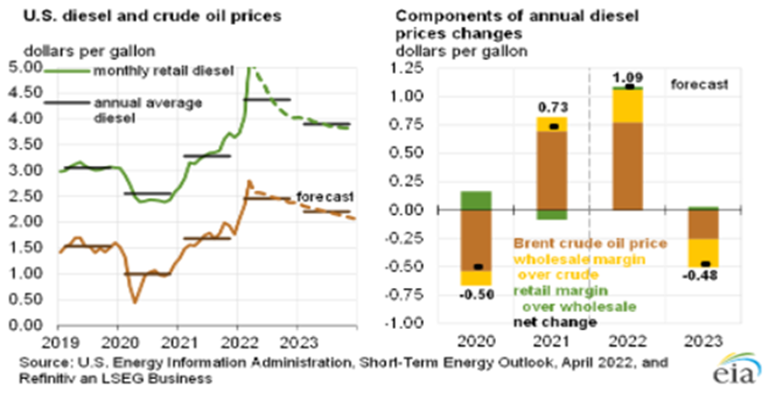

In the wake of war in Europe, diesel prices posted their largest and second largest weekly increases ever in March, surging nearly $1.15 in just two weeks. The 74.5- cent spike during the week ended March 7 resulted in a record national average price surpassing one that had stood since July 2008. A 40.1-cent increase the following week broke that record at $5.25 a gallon. Diesel prices then eased but are still within 11 cents of the record.

The Brent crude oil spot price averaged $117 per barrel (b) in March, a $20/b increase from February. Crude oil prices increased following the further invasion of Ukraine by Russia. Sanctions on Russia and other actions contributed to falling oil production in Russia and created significant market uncertainties about the potential for further oil supply disruptions. These events occurred against a backdrop of low oil inventories and persistent upward oil price pressures.

U.S. crude oil production in the forecast averages 12.0 million b/d in 2022, up 0.8 million b/d from 2021. We forecast production to increase another 0.9 million b/d in 2023 to average almost 13.0 million b/d, surpassing the previous annual average record of 12.3 million b/d set in 2019.

Modal Update

Logistics News Flash:

Solid Import Volumes Are Still Flowing Through Port of Long Beach

The head of the U.S.’s second-busiest container seaport said he has seen no letup in import volumes, though there may be some slowing in coming months as high inflation and growing services spending threaten to temper consumer demand for goods.

Port of Long Beach Executive Director Mario Cordero said the March total for containers moving through the port is looking “pretty good” and will be announced in the next couple of days.

Long Beach and its slightly busier neighbor, the Port of Los Angeles, handle more than 40% of all container traffic into the U.S. The San Pedro Bay docks have faced congestion and equipment shortages as a crush of consumer goods caused queues to form off the coast. While the number of waiting ships has dropped by two-thirds from a record in January, Russia’s invasion of Ukraine and soaring inflation are adding uncertainty to still-stretched global supply chains.

Meanwhile, lockdowns in Shanghai, Shenzhen and other cities in China have led to growing bottlenecks off its coast, threatening more delays in merchandise shipping and higher freight rates in coming months. A potential whiplash of goods heading into the U.S. risks another snarl as factories and logistics operations emerge from those shutdowns.

Cordero said he’s watching the Covid-19 situation in China closely as the Asian country struggles with an outbreak that’s locked down two major cities. Cordero said he’s keeping an especially close eye on Shenzhen’s Yantian port, as many of its container's transit through Southern California gateways.

“We’re going to monitor this for next couple of weeks to see how extensive that shutdown is” and whether China can control the outbreak, Cordero said. “We’ll go from there, but I myself, yes, I am concerned.”

Cordero said the surge in inflation could cool U.S. consumer demand, though he hasn’t seen evidence of that at the port yet. In addition, he’s watching for Americans to boost spending on services and entertainment, potentially hitting spending on goods, while Russia’s war in Ukraine is also a “disruptor to the global supply chain.”

Source for full article: https://www.bloomberg.com/news/articles/2022-04-07/west-coast-port-chief-says-import-volumes-held-up-in-march

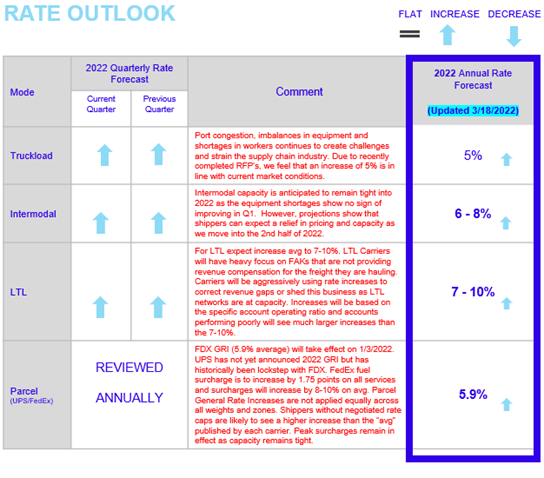

Rate Outlook Updates: Contract LTL, Truckload and Intermodal

The outlook for LTL rates is a 5.8% increase y/y in 2022, up from 2.4% previously.

FTR forecasts truckload rate outlook indicates a stronger increase for 2022, but the principal factor is a small downward revision in the 2021 data. The revision puts 2021 truckload rates up 18.4% from 2020 rather than the 19.2% gain previously. Truckload rates are forecast at 4.5% higher y/y in 2022.

The outlook for intermodal rates increased slightly this month with rate increases not expected to be flat with 2021 levels until December. Last month, they were expected to reach flat in the late third quarter.

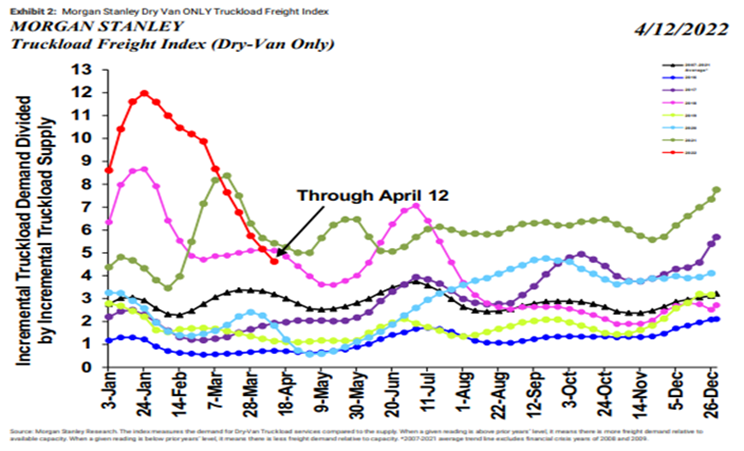

Morgan Stanley Index

We saw “red” across the board this week as our TLFI, and Reefer/Flatbed Indices all declined sequentially and underperformed typical seasonality. However, the magnitude of underperformance has appeared to begin to level off after peaking in March. At the underlying levels, the demand and supply components of our TLFI missed typical seasonal trends by ~800 bps and ~500 bps respectively (compared to ~1,900 bps and ~1,300 bps during our last update). Sequentially, the demand component declined by ~1,230 bps while the supply component increased by ~900 bps. With this update the index remains below 2021 levels and has now moved under 2018 levels but remains comfortably above LT averages.

Cass TL Linehaul Index (April 2022)

The Cass Truckload Linehaul Index® rose 14.2% y/y in March to 163.4 after rising 12.7% y/y in February to 158.0. We recently refined the data set to improve its reflection of the market, and the March increase is consistent with other contract rate sources. Just as this index is catching up, the key leading indicators from the truckload spot market have fallen sharply over the past several weeks, which we expect will limit further upside in the Cass Truckload Linehaul Index. Normal contract timing would suggest there’s room for this index to continue to rise for a few more months after the peak in spot rates.

Parcel Update:

Understanding New USPS Shipping Fees

The United States Postal Service introduced yet another set of new shipping fees on April 3, 2022. So, what does this mean for you and your business?

What are the new USPS shipping fees?

USPS had originally planned to kick off the new year with its new shipping rates, but instead graciously decided to postpone the implementation until April 3, 2022 to give customers more time to adjust to the changes. The main reason behind the raise in rates is to make it easier for USPS to manage manual handling costs, specifically when package dimensions exceed its sortation requirements.

These new nonstandard fees will affect both domestic retail and commercial mail that falls into any of the following categories: Priority Mail Express, Priority Mail, First-Class Package Service, USPS Retail Ground, and Parcel Select.

The surcharges will apply to packages that exceed certain dimensions. Here’s the breakdown:

- Packages longer than 22 inches: $4

- Packages longer than 30 inches: $15

- Packages longer than 2 cubic feet: $15

On the bright side, if you’re shipping Flat Rate products, Regional Rate products, or returns, these new shipping rates won’t apply.

What do the new USPS shipping fees mean for you?

While USPS increasing its shipping fees may not come as a surprise, it’s still important to be aware of exactly how these surcharges will affect you—especially when it comes to how quickly the fees can add up over time.

For example, if you’re sending packages that are 24 x 8 x 4”, a common long corrugated box, you’ll need to pay $4 per box because the packages are longer than 22 inches. However, let’s say you also have a package that’s 24 x 12 x 12”. You would not only have to pay the $4 for the length of the package, but because this box is also more than 2 cubic feet, you’d need to pay another $15, bringing your total to $19 in surcharges, just for one box.

Source for full article: https://parcelindustry.com/article-5882-Understanding-New-USPS-Shipping-Fees.html

Current LTL Market:

XPO Chairman Jacobs says Transportation Economy Shows Signs of Slowing

XPO Logistics Inc. CEO Brad Jacobs said that the transportation-specific economy remains strong but is slowing and not as vibrant as it was earlier in the year.

Jacobs, also chairman of the Greenwich, Conn.-based carrier, made his comments during a presentation at the Economic Club of New York on April 13.

He also noted that international events, including Russia’s invasion of Ukraine and the possibility of a slowing U.S. economy, higher interest rates and rising inflation, are causes for concern.

“Fasten your seat belt and tighten up. We’re in a place where the future is not very clear what is going to happen. In the supply chain, you look at truckload rates, what’s the price to transport a full truckload of freight from point A to point B, and they’re down 30% in the last month. That’s a huge move in a few weeks,” Jacobs said. “There’s been a shift in supply and demand. There are still elevated prices, but it’s not as strong as it was 30 days ago.”

He also said other trucking-specific indicators point to a slowing freight market.

“You look at the load-to-truck ratio, how many shipments are there for every truck that is available. That was about 11-to-1 just a few months ago, and now it’s down to 4-to-1,” Jacobs said. “You look at tender rejection rates, and you can look at them to tell how tight the market it is. They’re down about 11% year-over-year, and they were down about 4% a year ago.”

The tender rejection rate is a measurement of carriers’ willingness to accept or reject the loads that are tendered to them by shippers.

Jacobs said as the pandemic eases, the consumer sector and industrial side of the economy remained strong, but he believes there are signs of slowing.

Source for full article: https://www.ttnews.com/articles/xpo-chairman-jacobs-says-transportation-sector-economy-showing-signs-slowing

Current Truckload Market:

Cass reports ‘freight slowdown’ in March

Freight shipments advanced in March but at a slower pace, according to data released from Cass Information Systems. Freight expenditures, however, continued upward at a blistering pace.

The volumes subset of the Cass Freight Index increased just 0.6% year-over-year in March, 300 basis points slower than the growth rate logged a month ago. The dataset was also 1% lower than February when seasonally adjusted.

“While a few points of softness in Q1 were due to omicron-related absenteeism, freight was slowing even before the war in Ukraine began,” ACT Research’s Tim Denoyer commented in the report.

First-quarter volumes slowed to a 0.4% year-over-year growth rate, after climbing 4.3% in the fourth quarter and 9.5% in the third quarter.

“The threat of freight recession has risen recently as services reopen, inflation presses up interest rates and — though war-related effects are likely to be modest in the near-term — higher energy prices have an increasingly negative effect over time,” Denoyer added. “We’re certainly seeing a freight slowdown and spot market correction, but in our view, it is too early to call it a freight recession.”

The dataset represents all domestic transportation modes but is heavily weighted to truckload (50%) and less-than-truckload (25%). The March report showing a cooling in demand comes as commentary and data points for the TL industry have skewed negative, the result of capacity bleeding back into the market and spot rates falling quickly.

The expenditures index jumped to a record level, up 33.2% year-over-year. Compared to March 2020, the index is 70% higher as freight expenditures have climbed 53% over that period with higher volumes making up the difference. Seasonally adjusted, expenditures dipped slightly from February.

The expenditures index is forecast to increase 25% in 2022 as the year-over-year comparisons stiffen. The outlook is based on “normal seasonality” for the remainder of the year. However, 2022 has been anything but normal as volumes remained elevated to start the year, falling in March when they normally improve.

Source for full article: https://www.freightwaves.com/news/cass-reports-freight-slowdown-in-march

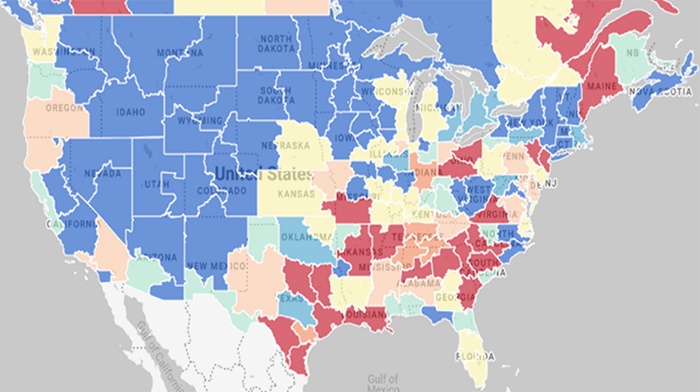

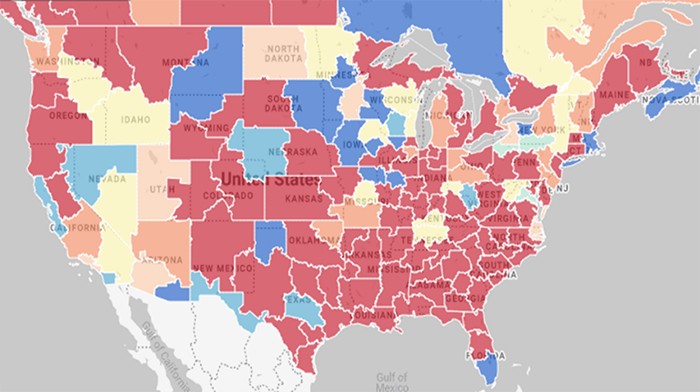

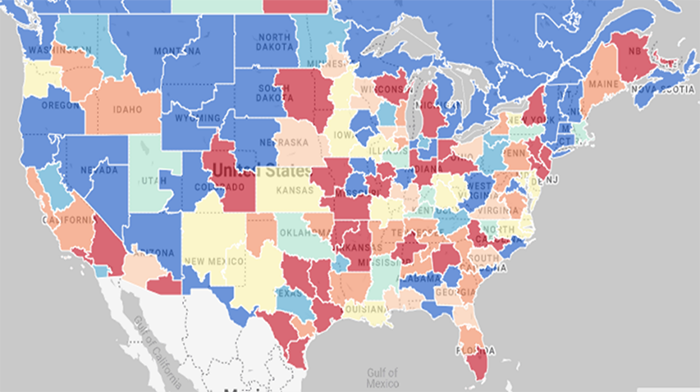

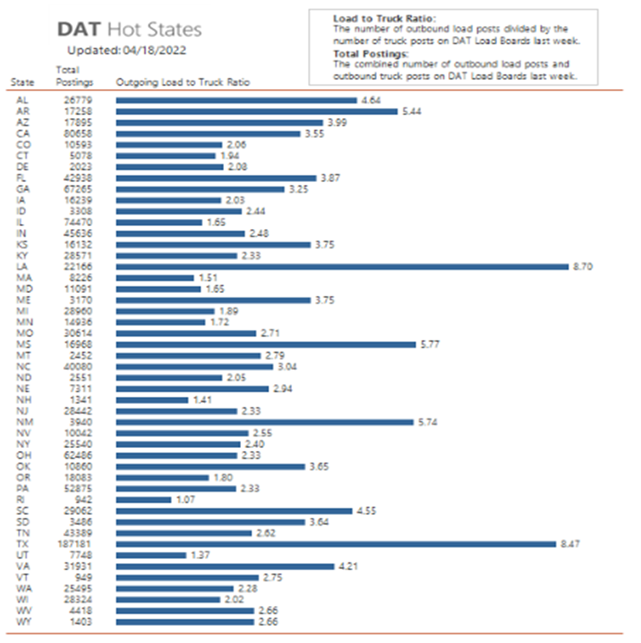

DAT Hot States: Vans, Flatbeds and Reefers

DAT Hot States for vans, flatbeds and reefers uses the MCI cool to hot, or -100 to +100, scale for measuring market temperature.

On the following maps of the U.S., when the market is cool (darker blue areas), capacity is loose and in the negative range. When the market is hot (darker red areas), capacity is tight and in the positive range. The lighter colored areas (including yellow) capacity is more neutral.

Vans – April 2022

Flatbeds – April 2022

Reefers – April 2022

The load to truck ratio from DAT is a strong indicator of the balance between demand and capacity. Changes in the ratio could mean changes in rates. The higher the ratio, the tighter the capacity is for a particular state. As of April 18, 2022, DAT Hot States, the state with the highest load to truck ratio was Louisiana (8.70) with Rhode Island (1.07) the lowest for the month.

Rate Outlook, Regulatory Update and Closing Thoughts

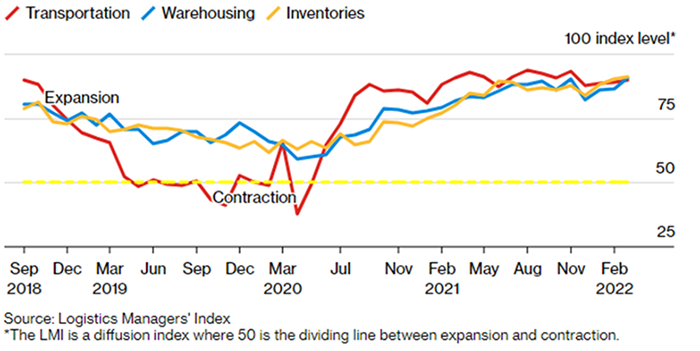

U.S. Supply-Chain Pressures Soar to a Record, Index Shows

A measure of U.S. supply-chain pressures rose to a record, adding to already stiff inflationary headwinds from logistics amid dwindling warehouse space and unprecedented inventory costs.

The Logistics Managers’ Index, released Tuesday, advanced for a third straight month in March, reaching 76.2 from 75.2 in February. The monthly survey, released by Colorado State University and affiliated with four other American universities, asks logistics managers about inventories, warehousing and transportation.

“Continued inventory congestion has driven inventory costs, warehousing prices, and overall aggregate logistics costs to all-time high levels,” the report stated. “This is putting even more pressure on already-constrained capacity.”

A Logistical Nightmare:

Transport, warehouse and inventory costs rose close to records in the U.S. Inventory levels dipped to 75.7 from February’s high of 80.2, though their costs rose to a record 91, according to the report. Warehouse capacity suffered a “a rather precipitous drop” in March, pushing prices for storage space to an all-time peak of 90.5. The report highlighted crosscurrents buffeting the U.S. economy, where accelerating inflation threatens to hurt consumer demand. Firms that boosted stockpiles during two years of pandemic-driven supply uncertainty, meanwhile, are trying to assess whether they’ve overbought or whether the added cushion is a more permanent feature. Inventory costs “are anticipated to remain very high throughout the next 12 months,” according to the report.

Transport Softness:

In the survey results, transportation prices were little changed from a month earlier, utilization rose and capacity edged higher -- perhaps not yet reflecting signs of weakness elsewhere in the second half of March that some analysts say portends a freight recession. While that’s possible, “there’s also a good chance it could lead to a moderation in prices that could end up being a relief in some sectors of the economy,” Zac Rogers, an assistant professor of supply-chain management at Colorado State, said in an email.

Source for full article: https://www.bloomberg.com/news/articles/2022-04-05/u-s-supply-pressures-soar-to-all-time-high-index-shows

Feds reject industry advise for under-21 truck driver progam

Federal regulators have rejected certain recommendations from trucking and safety groups on its CDL pilot program for those ages 18-21 as regulators work to keep the project on track before a White House approval deadline.

The Federal Motor Carrier Safety Administration stated it is turning down advice from the American Trucking Associations and others that the agency do away with a requirement that carriers participating in FMCSA’s Safe Driver Apprenticeship Pilot (SDAP) also join the U.S. Department of Labor’s registered apprenticeship program.

DOL’s program, part of the Biden administration’s Trucking Action Plan, just completed a 90-day Apprenticeship Trucking Challenge to jump-start carrier apprenticeships as a way to boost the trucking industry’s driver ranks.

In comments filed with FMCSA earlier this year, ATA noted that while it supports both the FMCSA and DOL apprenticeships, many carriers may not want to sign up for the DOL program because of the added costs. ATA also pointed out that requiring carriers to sign on to the DOL apprenticeship in order to be part of FMCSA pilot was not required under the federal infrastructure law authorizing FMCSA’s program.

Source for full article: https://www.freightwaves.com/news/feds-reject-industry-advice-for-under-21-truck-driver-program

Closing Thoughts

Economy

With COVID restrictions for travel loosening, many people are moving their spending away from products and moving more toward leisure spending. This has caused the freight market to loosen a little bit for the first time since the pandemic started in 2020. However, with the continued Chinese lock downs many worry that supply chain issues and higher inflation will continue later into 2022. With many goods stuck in the ports of China, once the ports open back up there will likely be a flood of freight coming out causing another wave of tightened ocean and air capacity. This would then be followed by another tightening of over the road capacity (OTR). OTR capacity will likely also start to tighten back up after the slight break as many U.S. carriers gear up for produce season.

Demand/Supply

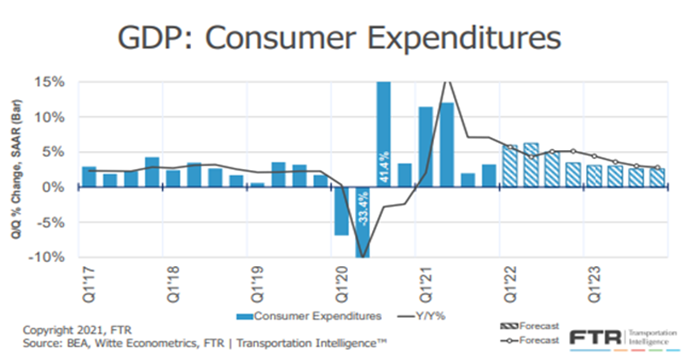

The issues faced in 2021 brought to light the need to focus investments on equipment, buildings and expenses. This has led to the increased production and more jobs and more spending. As things begin to normalize, personal consumption expenditures dropped severely from 7.9% to 3.5%; this continues to be driven by the many uncertainties of the Ukraine crisis, inflation, and the remaining effect of COVID 19. The GEODIS team will continue to monitor the trucking market to confirm if performance is due to delayed seasonality, related to COVID lockdowns in China and/or something more ominous. We will also be using this drop to take advantage of the softening market to reduce transactional freight costs for our customers.

We hope you enjoyed the latest GEODIS Industry Update digest and found it useful and informative. Please subscribe to receive future Industry Updates each month.

by

by