JANUARY 2022 GEODIS INDUSTRY UPDATE DIGEST

24/02/2022

24/02/2022Welcome to the January 2022 GEODIS Industry Update digest

Our monthly Industry Update provides the latest nationwide economic data, fuel-related concerns, modal rate outlooks, indexes as well as a variety of additional statistics and news items to provide a broad overview of what’s impacting the U.S. transportation industry nationally and globally.

Economic Overview

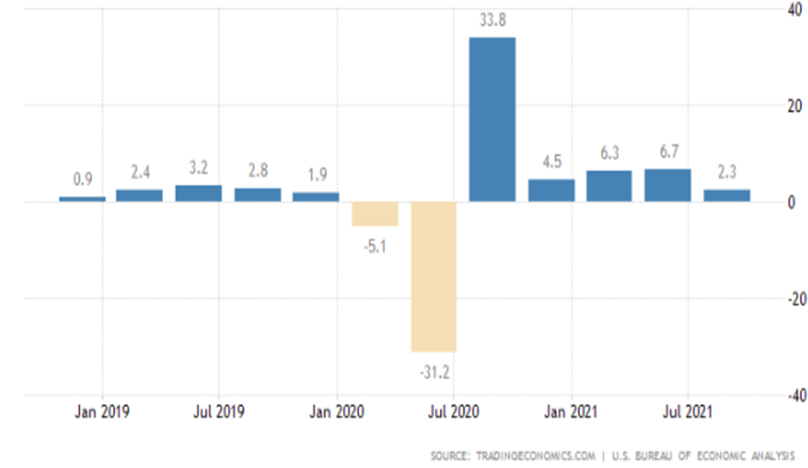

GDP

The U.S. economy grew by an annualized 2.3% on quarter in Q3 2021, slightly higher than 2.1% in the second estimate and following a 6.7% expansion in the previous three-month period. The update primarily reflects upward revisions to personal consumption expenditures (2% vs 1.7% in the second estimate) and private inventory investment (12.4% vs 11.6%) that were partly offset by a downward revision to exports (-5.3% vs -3%). Meanwhile, imports were revised down (4.7% vs 5.8%).

U.S. Trade Deficit (November 2021)

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $80.2 billion in November, up $13.0 billion from $67.2 billion in October, revised. November exports were $224.2 billion, $0.4 billion more than October exports. November imports were $304.4 billion, $13.4 billion more than October imports.

Unemployment Rate

The U.S. Bureau of Labor Statistics reported that nonfarm payroll employment rose by 199,000 in December, and the unemployment rate declined to 3.9 percent. Employment continued to trend up in leisure and hospitality, in professional and business services, in manufacturing, in construction, and in transportation and warehousing.

Labor Participation Rate

The labor force participation rate in the U.S. was unchanged at 61.9 percent in December 2021, remaining still 1.5 percentage points lower than in February 2020 before the pandemic started.

Manufacturing

The ISM manufacturing index decreased to 58.7 in December from 61.1 in November. There was a modest slowing of the growth in new orders and production. The index components related to prices and supplier deliveries saw notable drops, suggesting continuing improvement in supply chain performance. The outlook for production is decent.

Consumer

Retail sales remained healthy in November, although growth was not as strong as October. Total sales increased 0.3% in November following a 1.8% advance in October. Performance was mixed in November with advances in gas stations, grocery stores, and sporting goods stores, and declines in department stores and electronics and appliance stores. The year-over-year rate increased to 18.2%, up from 16.3% in October.

Residential Construction

New residential investment increased more than expected in November. Housing starts increased by 11.8% in November to an annual pace of 1.68 million. Single-family starts leaped 11.1% to an annual pace of 1.17 million. The multi-family sector saw starts at 491,000. Future activity looks good as total permits rose 3.6% to 1.712 million.

Fuel Forecasts and Trends

FTR Fuel Outlook

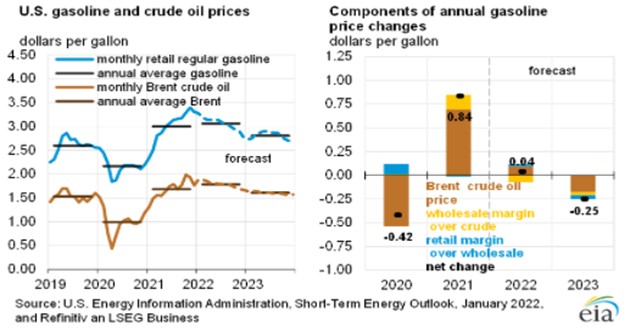

After rising 41 cents from late August through mid-November – mostly in October – diesel prices declined about 12 cents over seven consecutive weeks in November and December. Crude prices have been holding steady in the range of $75 per barrel.

U.S. regular gasoline retail prices averaged $3.02 per gallon (gal) in 2021, compared with an average of $2.18/gal in 2020. We forecast gasoline prices will average $3.06/gal in 2022 and $2.81/gal in 2023. U.S. diesel fuel prices averaged $3.29/gal in 2021, compared with $2.56/gal in 2020, and we forecast diesel prices will average $3.33/gal in 2022 and $3.27/gal in 2023.

U.S. crude oil production averaged 11.2 million b/d in 2021. We expect production to average 11.8 million b/d in 2022 and to rise to 12.4 million b/d in 2023, which would be the highest annual average U.S. crude oil production on record. The current record is 12.3 million b/d, set in 2019.

Modal Update

Logistics News Flash:

Teen Truckers Soon to Get Interstate Nod to Help Supply Chain

Teenage truck drivers will soon be allowed to drive across state lines under a pilot program the Transportation Department is advancing.

Recently enacted infrastructure law included apprenticeships that will let people as young as 18 drive trucks interstate, an idea pitched as a way to help alleviate nationwide delays in the supply chain of goods. One trade group, the American Trucking Associations, has estimated that the industry is short 80,000 drivers.

The Federal Motor Carrier Safety Administration revealed details of the pilot apprenticeship program in an information collection request set to publish Friday. Public comment must be submitted within five days. The law (Public Law 117-58), signed in November, requires the department to establish the program within 60 days of enactment.

Under the program, 18- to 20-year-olds will be allowed to operate trucks in interstate commerce supervised by an experienced driver for two probationary periods, totaling no less than 240 driving hours. The apprentice then could drive without an experienced driver, according to the regulation. Motor carriers in the program will need to submit monthly crash, inspection, safety and exposure data.

Source for full article: https://news.bloomberglaw.com/daily-labor-report/teen-truckers-soon-to-get-interstate-nod-to-help-supply-chain

Struggling Supply Chain Managers Confront Escalating Transport Rates in 2022

Supply Chain Managers Struggling

Irrespective of mode, rates will be escalating, with carriers controlling capacity and exercising leverage like never before.

Given the shortage of manpower and labor pools across the spectrum of global logistics, supply chain managers will be struggling.

Crafting an annual rate forecast has never been easier. Soaring inflation, tightening cargo capacity, and a shrinking labor market only add up to one thing for today’s global logistics managers: the triple whammy. Industry analysts advise supply chain managers to expect a steady escalation of rates and expenses.

Trucking: Hang in There

Satish Jindel, principal of SJ Consulting – which closely tracks the less-than-truckload (LTL) sector – advises logistics managers to begin analyzing truckload (TL) pricing because it has implications for intermodal as well. Furthermore, it’s by far the largest market in domestic freight transportation.

He also notes that despite disruptions from the coronavirus and resulting changes in demand levels from shippers, leading LTL companies are able to gain rate increases in the mid-to-high single digits due to tight capacity.

“And that is needed by carriers,” he says. “Shippers should realize that these increases are helping transport providers reinvest in drivers, equipment, and technology needed to support the demand.”

According to Jindel, shippers can save on total transportation spending with more rather simple tactical planning that requires getting rid of some past practices.

Rail & Intermodal: Boom and Bust

Rate Forecasts are always challenging for this sector, says Jason Kuehn, vice president of the consultancy Oliver Wyman. But this one feels more difficult than most.

“Rail and intermodal pricing were very strong this year,” he says. “Demand was robust this year and truck shortages and supply chain congestion slowed things downing creating a perfect storm for logistics shortages.”

But with all things that boom, there usually follows a bust, Kuen maintains. Inflation is high and consumer sentiment is declining. He adds that after a strong year and an all-out back in-person Holiday season, consumer spending may see a pull-back in 2022.

“Grocery, gas, restaurant prices – and soon – utility bills are all going to be higher tugging at the consumer wallets,” says Kuen. “Input expenses are also soaring for iron and steel scrap, finished steel, oil and natural gas, and wage rates. It seems unlikely that people can absorb these increases without some retrenchment in demand. It has been a long time since we have seen 5+% inflation rates.”

Source for full article: https://www.supplychain247.com/article/struggling_supply_chain_managers_confront_escalating_transport_rates_2022/smc3?oly_enc_id=5801B4487478I0Y

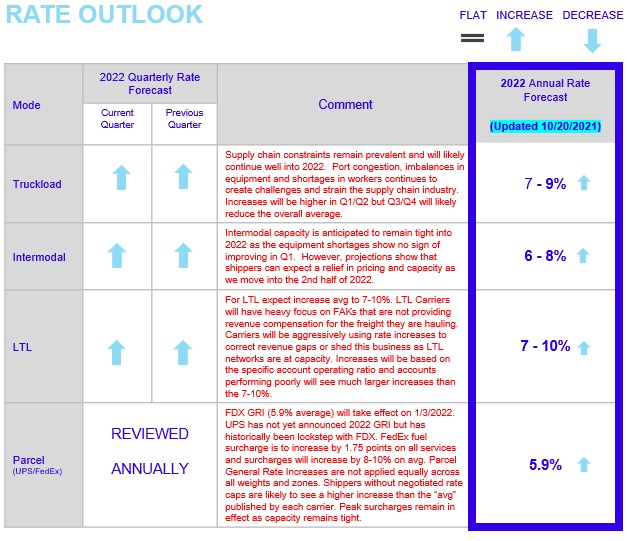

Rate Outlook Updates: Contract LTL, Truckload and Intermodal

The outlook for LTL rates is an increase of 0.7% in 2022 following the estimated 2021 increase of about 17%.

The truckload rate forecast for 2022 is slightly stronger at 2.7% higher y/y, excluding fuel. Contract rates look to rise nearly 6% as spot rates are forecast to decline only 2.5%.

Intermodal rate increases are expected to be much more muted in 2022 than they were in 2021. It is expected that intermodal rate increases will turn negative in the final quarter of 2022, compared with where they were during the final quarter of 2021.

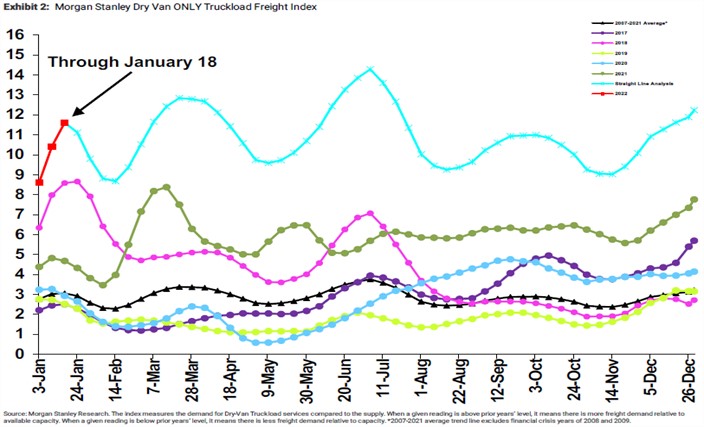

Morgan Stanley Index

The Morgan Stanley index reaches all-time high. Continuing the strong run the index saw in 2021, our TLFI continued to push upward in the first few weeks of 2022 and reached the highest level we’ve seen since the inception of the index. The underlying supply and demand components both outperformed and contributed to the overall index’s gains. The demand component increased sequentially and outperformed seasonality by ~2,000 bps while the supply component decreased sequentially and outperformed seasonality by ~2,600 bps.

Cass TL Linehaul Index (December 2021)

The U.S. transportation sector delivered in time for the holidays as the shipments component of the Cass Freight Index® accelerated to 7.7% y/y growth in December from 4.5% in November. Though virtually unchanged m/m, the Cass shipments index jumped 4.2% from November to December on a seasonally adjusted (SA) basis, as shipment volumes held firm despite the normal holiday slowdown. Though the record backlog of 105 containerships off Southern California and sharp declines in intermodal volumes in early 2022 still demonstrate capacity constraints on freight volumes, the strong finish to 2021 shows progress as the trucking industry has begun to build driver and equipment capacity despite extraordinary challenges.

Parcel Update:

FedEx warns of shipment delays as Omicron leads to staffing shortage

FedEx Corp (FDX.N) warned on Friday that rising cases of Omicron variant has caused staff shortage and delay in shipments transported on aircraft.

"The explosive surge of the COVID-19 Omicron variant has caused a temporary shortage of available crew members and operational staff," the company said.

The delivery firm said severe winter storms around the country, including at its main air hub in Memphis, Tennessee, are posing challenges and it is implementing contingency plans and adjusting operations to minimize disruptions.

Rival United Parcel Service Inc (UPS.N) said that call-outs due to Omicron are not impacting their services, adding that contingency plans are in place.

Source for full article: https://www.reuters.com/markets/commodities/fedex-warns-shipment-delays-omicron-leads-staffing-shortage-2022-01-07

Current LTL Market:

Supreme Court blocks COVID vaccine mandate for large businesses

With the trucking sector having in hand fresh guidance from the federal government that the Biden administration’s workplace vaccination/testing rules don’t apply to solo truck drivers, the rule for now is dead anyway.

The Supreme Court Thursday afternoon handed down a 6-3 decision that the rule promulgated by the Occupational Safety and Health Administration cannot be enforced and is likely to be rejected in further court action. Some parts of the rule regarding mask wearing went into effect Monday, but a series of earlier court battles had left its status unclear before Thursday’s Supreme Court ruling.

While solo drivers may not have been facing the mandate, the guidance handed down by OSHA in the past few days made clear that the rules would apply to team drivers. Now, they no longer need to be concerned about them.

The American Trucking Associations was one of the many plaintiffs in the case and celebrated the ruling.

Source for full article: https://www.freightwaves.com/news/breaking-news-supreme-court-blocks-covid-vaccine-mandate-for-large-businesses

Christenson Transportation acquires family-owned Sharp

Christenson Transportation announced Monday that it is expanding its freight network with the recent acquisition of Sharp Transport Inc. The acquisition of family-owned Sharp Transport, headquartered in Ethridge, Tennessee, which has approximately 120 drivers, including a mix of company drivers and owner-operators, brings the Strafford, Missouri-based Christenson Transportation fleet to nearly 300 drivers and will add around 240 tractors and 940 trailers.

Financial terms of the transaction were not disclosed, but the acquisition was finalized on Dec. 31.

Don Christenson, president and CEO of Christenson Transportation, told FreightWaves in an exclusive interview that his family-owned company passed on acquiring four or five companies in 2021 before entering into talks with Sharp Transport about buying its trucking and brokerage operations.

“We found Sharp Transport late in the year but from our initial meeting with the Sharp family, we knew that their driver culture was similar to ours and that was really important to us,” Christenson told FreightWaves.

Source for full article: https://www.freightwaves.com/news/exclusive-christenson-transportation-acquires-family-owned-sharp

LA port pressures ocean carriers to remove empty containers faster

In its latest congestion mitigation effort, the Port of Los Angeles announced Thursday it plans to start charging ocean carriers a hefty surcharge next month for empty containers that are stored on marine terminals for nine days or longer.

Under the new program, scheduled to go into effect Jan. 30, carriers will be billed $100 per empty that overstays the limit, with the fee increasing in $100 increments per container per day until the container departs the terminal.

The fees proposed by port authority staff are subject to approval by the Los Angeles Harbor Commission. The next scheduled board meeting is on Jan. 13.

Whether the new fee will help declutter the port more than a similar $100 fee schedule on import containers is unclear. The import storage fee was approved at the end of October but has been postponed for seven consecutive weeks because of some progress in reducing long-stored containers.

The proposed fine is designed to motivate carriers to relocate idle boxes, but Matt Schrap, CEO of the Harbor Trucking Association, noted that carriers might comply by further restricting empty returns to avoid the fee if a scheduled vessel arrival is longer than nine days and then charge road haulers a daily late fee to store the empties for them. “It cuts both ways,” he said in an email.

Source for full article: https://www.freightwaves.com/news/la-port-pressures-ocean-carriers-to-remove-empty-containers-faster

DAT Hot States: Vans, Flatbeds and Reefers

DAT Hot States for vans, flatbeds and reefers in December — using the MCI cool to hot, or -100 to +100, scale for measuring market temperature — is trending toward “hot” in all three sectors. When the market is cool, capacity is loose and in the negative range. When the market is hot, capacity is tight and in the positive range.

The load to truck ratio from DAT is a strong indicator of the balance between demand and capacity. Changes in the ratio could mean changes in rates. The higher the ratio, the tighter the capacity is for a particular state. As of January 17, 2022 DAT Hot States, the state with the highest load to truck ratio was Wyoming by far at 27.78 and the lowest Florida at 4.25.

Rate Outlook and Regulatory Update

Omicron, Inflation Drive Down U.S. Growth Outlook

The outlook for economic growth in the first quarter and 2022 is darkening amid the latest wave of Covid-19, as consumers grapple with high inflation and businesses juggle labor and production disruptions.

Forecasters surveyed by The Wall Street Journal this month slashed their expectation for growth in the first quarter by more than a percentage point, to a 3% annual rate from their forecast of 4.2% in the October survey.

The combination of higher inflation, supply-chain constraints and the fast-spreading Omicron variant caused economists to trim their forecast for growth to 3.3% for the current year as a whole, based on the change in inflation-adjusted gross domestic product in the fourth quarter of 2022 from a year earlier, from 3.6% in October. Last year, output rose 5.2%, economists estimate.

The economy faces a delicate balancing act this winter, economists say, as the rapid spread of the Omicron variant threatens to dent consumer spending and exacerbate labor and supply-chain shortages as workers call out sick.

Source for full article: https://www.wsj.com/articles/omicron-inflation-drive-down-u-s-growth-outlook-11642345202

New Vaccine Rules Take Effect at Canadian Border

As of Jan. 15 new, tougher COVID-19 vaccine requirements took place for people to cross from the U.S. into Canada. That applies to truck drivers and other essential workers.

It is expected similar requirements will take effect in the U.S. on Jan. 22 as the Department of Homeland Security implements its requirements to prevent the spread of the coronavirus and encourage more people to become vaccinated.

“On Nov. 19, 2021, we announced that as of Jan. 15, 2022, certain categories of travelers who are currently exempt from entry requirements will only be allowed to enter the country if they are fully vaccinated with one of the vaccines approved for entry into Canada,” said a Jan. 13 statement from the Canadian Ministry of Transport and Ministry of Public Safety. “These groups include several essential service providers, including truck drivers. Let us be clear: This has not changed. All drivers and truck drivers going into Canada will have to show proof of vaccination in order to be able to go into Canada, whether they’re an essential worker or not.”

Source for full article: https://www.ttnews.com/articles/new-vaccine-rules-take-effect-canadian-border

Closing Thoughts: Economy and Demand/Supply

Economy

Now that we are well into December, the holiday shopping season is nearing the finish line. The question remains how have the existing factors fluctuating from economic indicators to the twists of the COVID-19 pandemic affected the season so far. Just before Thanksgiving, the Bureau of Economic Analysis released data showing that U.S. economic growth slowed to a modest 2.1% in the third quarter.

Demand/Supply

The global supply chain disruptions may continue well into 2022 as experts are forecasting. Measures to contain COVID-19 can affect manufacturing and shipping operations, which is exacerbating an already depleted supply chain crisis. With the newest COVID-19 variant, Omicron, becoming the latest obstacle, many workforces continue to rev up. Production shortfalls are behind the current contraction in global trade volume, but logistic bottlenecks are hindering the total output.

We hope you enjoyed the latest GEODIS Industry Update digest and found it useful and informative. Please subscribe to receive future Industry Updates each month.

by

by