MAY 2022 GEODIS INDUSTRY UPDATE

08/06/2022

08/06/2022Welcome to the May 2022 GEODIS Industry Update digest

Our monthly Industry Update provides the latest nationwide economic data, fuel-related concerns, modal rate outlooks, indexes as well as a variety of additional statistics and news items to provide a broad overview of what’s impacting the U.S. transportation industry nationally and globally.

Economic Overview

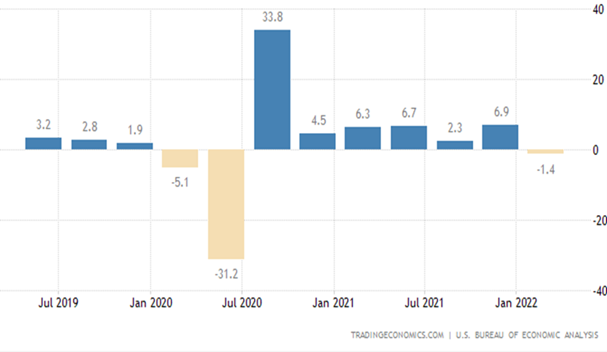

GDP

The American economy contracted an annualized 1.4% on quarter in the first three months of 2022, well below market forecasts of a 1.1% expansion and following a 6.9% growth in Q4 2021, primarily due to a record trade deficit and a decline in inventory investment. Exports dropped 5.9% (from 22.4% in Q4), while imports surged 17.7% (from 17.9% in Q4).

U.S. Trade Deficit (May 2022)

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced that the goods and services deficit was $109.8 billion in March, up $20.0 billion from $89.8 billion in February, revised. March exports were $241.7 billion, $12.9 billion more than February exports. March imports were $351.5 billion, $32.9 billion more than February imports. The March increase in the goods and services deficit reflected an increase in the goods deficit of $20.4 billion to $128.1 billion and an increase in the services surplus of $0.4 billion to $18.3 billion.

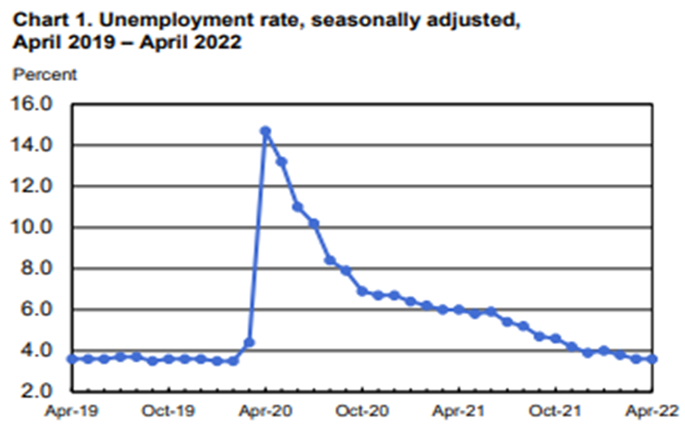

Unemployment Rate

The U.S Bureau of Labor Statistics reported that nonfarm payroll employment increased by 428,000 in April, and the unemployment rate was unchanged at 3.6 percent. Job growth was widespread, led by gains in leisure and hospitality, in manufacturing, and in transportation and warehousing.

Labor Participation Rate

The labor force participation rate in the US fell to 62.2 percent in April 2022 from 62.4 percent in March, the lowest in three months. The labor force participation rate remains 1.2 percentage points below its February 2020 values.

Manufacturing

The ISM manufacturing index in April decreased by 1.7 percentage points to 55.4, which is the lowest reading since July 2020. The index components most closely associated with demand for freight transportation – production and new orders – declined very slightly. The largest negative was slowing growth in employment.

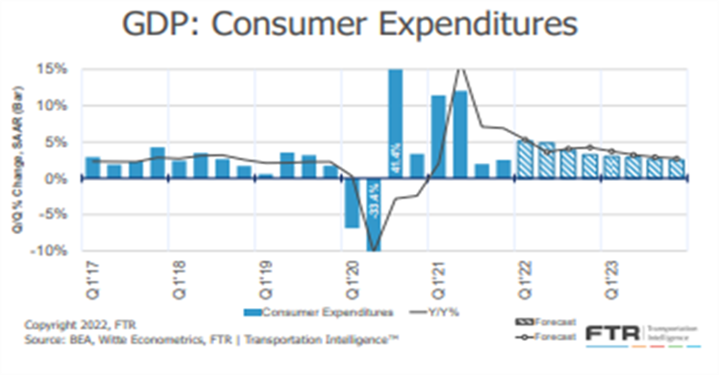

Consumer

Retail sales increased 0.5% in March and were up 6.9% from a year earlier. Gasoline sales accounted for most of the increase in sales in March, up 8.9%. Motor vehicle and parts dealers saw a 1.9% decline. Excluding vehicles and gasoline, sales were only up 0.2%, suggesting lower discretionary spending to pay for higher energy costs and rising interest rates on mortgages and credit cards.

Residential Construction

New home building rose in March but starts for single family housing fell, indicating that rising mortgage rates may be starting to cool the market. Housing starts increased 0.3% to a seasonally adjusted annual rate of 1.793 million last month. Single-family starts dropped 1.7% while the multi-family sector jumped 7.5%.

Fuel Forecasts and Trends

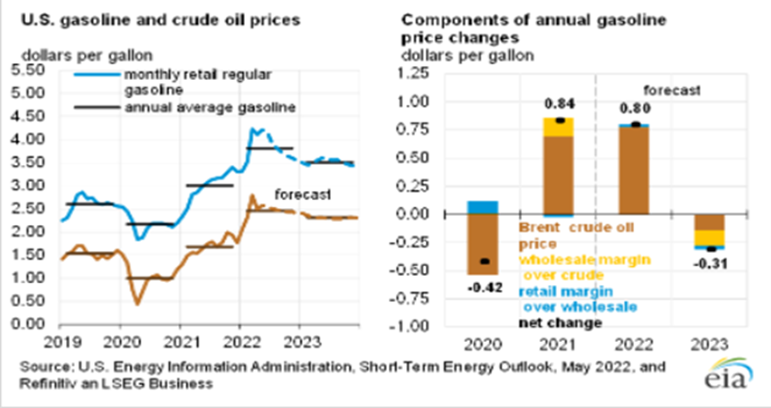

After the record surge in diesel prices in March, which had resulted in a record of $5.25 a gallon, it appeared that prices were settling in at a level between $5.10 and that record. Then came the week ended May 2, which saw a 34.9-cent jump – the third largest ever – to $5.509 a gallon. Distillate inventories are the lowest in more than seven years, and crude remains above $100 a barrel.

The Brent crude oil spot price averaged $105 per barrel (b) in April, a $13/b decrease from March. Although down from March, crude oil prices remain above $100/b following Russia’s full-scale invasion of Ukraine. Sanctions on Russia and other independent corporate actions contributed to falling oil production in Russia and continue to create significant market uncertainties about the potential for further oil supply disruptions.

U.S. crude oil production in the forecast averages 11.9 million b/d in 2022, up 0.7 million b/d from 2021. We forecast that production will increase to more than 12.8 million b/d in 2023, surpassing the previous annual average record of 12.3 million b/d set in 2019.

Modal Update

Logistics News Flash:

Record Diesel Prices Pressure European Drivers, U.S. Deliveries

An extended surge in diesel prices is challenging Wall Street bets that inflation is easing.

A global shortfall of the fuel—the workhorse for much of the world economy—is straining industries from trucking to farming and adding to the pressure consumers face from higher energy prices. Europe, dependent on imports of Russian diesel that are expected to slump because of sanctions, is particularly vulnerable.

Motorists and businesses are feeling the pinch. In the U.S., national average retail diesel prices rose to an all-time high for a 15th straight day on Friday, reaching $5.56 a gallon, according to AAA. They have shot up 56% in 2022, outstripping gains in the benchmark price for crude oil. Retail unleaded gasoline prices have risen 35% to a national average of $4.43 a gallon.

Diesel is used in the U.S. mostly in trucks, which means higher prices add to shipping and delivery costs. Inventories of distillates, which also include heating oil, fell recently to a 17-year low in the midst of lower refining activity and higher demand domestically and abroad, according to the U.S. Energy Information Administration. Supplies are particularly tight along the East Coast, where inventories have dropped to their lowest level since at least 1990.

In Europe, where diesel cars account for a bigger chunk of the auto fleet, prices in the wholesale market have leapt 88% over the past year. The availability of fuel is likely to worsen as sanctions on Russia tighten, exposing a flaw in the region’s energy setup.

Governments in recent decades pushed drivers to adopt diesel cars but didn’t upgrade the refinery industry so it could produce the fuel in greater quantities. That meant buying more diesel from Russia, the energy superstore on Europe’s doorstep.

Helge Ippendorf, chief executive of Via Logistik GmbH, a company based near the German city of Cologne that trucks artwork, road-safety materials and other wares, is shelling out 4,000 euros, the equivalent of $4,150, a week for diesel, 80% more than a year ago. He can’t remember such a jump in fuel prices since the 1970s oil shocks.

“No other impact in my whole career—and I started my own company in 1981—was as massive as the situation at the moment,” he said.

Rising energy prices are a major factor contributing to the persistence of inflation, which has sparked steep declines in the stock and bond markets. The S&P 500 fell 1.6% Wednesday after a gauge of U.S. consumer prices came in higher than Wall Street expected.

Source for full article: https://www.wsj.com/articles/record-diesel-prices-pressure-european-drivers-u-s-deliveries-11652416873?mod=djemlogistics_h

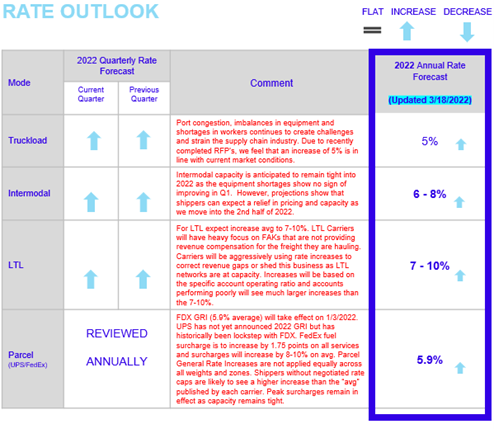

Rate Outlook Updates: Contract LTL, Truckload and Intermodal

The outlook for LTL rates is a 6.2% increase y/y, up from 5.8% previously. The 2023 forecast is a 5.6% decrease.

The truckload rate outlook is slightly weaker than in the prior forecast at a 3.8% y/y increase, down from 4.5%. The forecast for 2023 is a 3.4% y/y decrease in rates. Spot rates in 2022 are forecast to be down about 2% y/y, which is sharper than in the previous outlook. The projected 7.5% increase for contract rates is marginally weaker than in the prior forecast.

Intermodal rate expectations were little changed in the latest month with a declining trend expected through the end of the year. While last year’s gains will not recur, growth will hold at present levels, approaching flat by the end of the year.

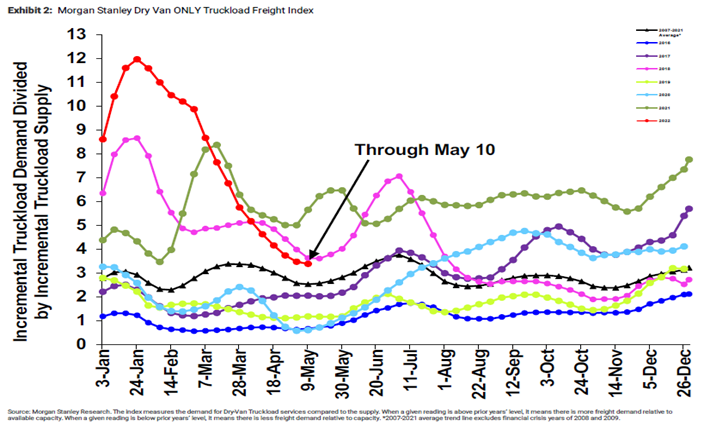

Morgan Stanley Index

Breaking the streak of underperformance that we have seen over the last several weeks, our TLFI moved ~inline with typical seasonality despite continuing to fall sequentially. This result follows three updates of improving second-derivative performance, as the magnitude of underperformance experienced by the index continued to level off from the peaks we saw in March (highlighted in our last update here). However, demand and supply both underperformed as the underlying components missed typical seasonal trends by ~800 bps and ~200 bps respectively. Sequentially, the demand component declined by ~580 bps while the supply component increased by ~360 bps. Performance in our other indices was also mixed with our Flatbed index underperforming and declining sequentially while our Reefer index performed ~inline despite declining sequentially.

Cass TL Linehaul Index (May 2022)

The shipments component of the Cass Freight Index fell 0.5% y/y, following a 0.6% y/y increase in March. Freight was slowing even before the war in Europe began, but the effects of the additional surge of inflation and recent interest rate increases seem to have push volumes over the edge. The prospect of freight recession is now considerable, as substitution from goods back to services spending picks up pace, and as inflation slows overall spending, particularly via higher fuel prices and by pressing up interest rates.

Parcel Update:

E-Commerce Blurs the Lines Between LTL and Parcel

The rise in e-commerce is resulting in transportation carriers redrawing networks and offering new services focusing on the last mile.

According to the US Census, total e-commerce sales for 2021 were estimated at $870.8 billion, an increase of 14.2% from 2020 and 44.7% from 2019. In terms of the last mile, the growth of e-commerce has come from both big and small packages.

Businesses are shipping smaller quantities of freight and parcels more frequently, giving logistics professionals more to manage in increasingly complex networks. And it's a pricey business for everyone involved.

Overwhelmed with the growth in big packages, UPS and FedEx implemented surcharges to mitigate costs associated with handling them. Small parcel sorting facilities are equipped to handle packages up to a specific size and width; however, as more big and bulky items such as exercise equipment, pet food, appliances, and home decorations were purchased online, less-than-trucking (LTL) providers stepped in.

"Retail is becoming a bigger part of LTL," which has historically drawn most of its freight from industrial sources, Satish Jindel, president of the consulting firm, Shipmatrix, told the Journal of Commerce in a 2021 interview.

Shipments that may have once required one truckload move are now being broken up into smaller quantities of freight that need to be moved more frequently. As such, there is a graying of the lines between parcel and LTL providers, and it starts in the middle mile.

Both types of providers require a strong fulfillment network close to the final customer. According to Jonathan Kletzel, transportation and logistics partner at consulting firm PwC, "I see LTL as being a critical enabler of local fulfillment for companies that want to compete with some of the national brands. To be successful, they will need to serve local fulfillment through more direct, smaller loads to be able to better manage local inventory, especially for slower-moving SKUs."

Source for full article: https://parcelindustry.com/article-5892-E-Commerce-Blurs-the-Lines-Between-LTL-and-Parcel.html

Current LTL Market:

Yellow Corp. says terminal closures won’t hurt freight capacity

Yellow Corp. expects to reduce the number of terminals in its network from 316 to 300 by year-end as the less-than-truckload carrier looks to further cut costs, company executives told analysts.

Speaking after Yellow reported first quarter financial results Tuesday, chief operating officer Darrel Harris said the terminal reduction would not affect the company’s ability to move freight.

“I just want to make it clear that we’re not giving up geographical coverage, and we’re also going to protect capacity for our customers because we do plan on growing when we complete One Yellow,” Harris said, referring to the company’s restructuring effort.

Yellow’s plan to close nine terminals emerged last week after it issued a notice to the Teamsters. The proposal also calls for the consolidation of 20 YRC Freight and Reddaway facilities and the realignment of ZIP codes in the West.

Yellow (NASDAQ: YELL) reported its best first quarter in six years after the market closed Tuesday. The period came in slightly better than breakeven on the operating line at a 99.3% operating ratio, which was 300 basis points better year-over-year. However, it reported a net loss of 54 cents per share, which was less than half the loss recorded in the 2021 first quarter but worse than the consensus estimate calling for a 41-cent-per-share loss.

A restructuring called “One Yellow” brought all of the company’s separately-run LTL carriers and logistics company onto the same tech platform. The next phase of the integration includes a terminal-by-terminal overhaul in the West.

In addition to the terminal rationalization, the change of operations also call for the addition of 11 velocity distribution centers, a new linehaul network and 260 utility driver positions.

Phase two is slated at carrier New Penn in the third quarter with phase three at carrier Holland taking place in the fourth quarter. When the process is complete, the carrier will be operating approximately 300 facilities. The changes will provide cost savings immediately on 28% of its network starting in the third quarter.

Source for full article: https://www.freightwaves.com/news/yellow-earnings-q1-2022

Current Truckload Market:

Cass reports ‘freight slowdown’ in March

Freight markets cooled in April, according to data provided by Cass Information Systems. “The prospect of freight recession is now considerable,” a Thursday report from the payments management provider read. Broad inflation, including higher diesel prices which impact the cost of everything shipped, interest rate hikes, and a transition in consumer buying habits to services from goods, drove the decline.

Freight shipments posted a modest dip in April, down 0.5% year-over-year, but a 3.5% decline from March (seasonally adjusted) is more likely to catch the eye of industry participants. The report cautioned that “more softness is on the horizon” as the comps get tougher in the coming months and the impact from production shutdowns in China is felt.

The blue-shaded area in the above graph is the National Truckload Index (linehaul only – NTIL), which is based on an average of booked spot dry van loads from 250,000 lanes and 10,000 daily spot market transactions. The NTIL is a seven-day moving average of linehaul spot rates excluding fuel. The green line represents the seven-day per-mile average rate for dry van contract loads excluding fuel.

“After a nearly two-year cycle of surging freight volumes, the freight cycle has downshifted with a thud, ACT Research’s Tim Denoyer commented. “It’s possible the April data include some indirect impact from lockdowns in China, but with container ship backlogs still off North American ports, the direct effects on finished goods imports seem more likely in the June/July timeframe.”

The downturn, however, is likely to be more pronounced for small carriers operating in the spot market. Numerous drivers obtained authority to operate on their own last year, buying equipment at record-high prices to chase record-high spot rates. The incremental capacity combined with a recent softening in freight demand has dented spot market fundamentals, making is a much tougher slog for the small operator working off load boards.

Source for full article: https://www.freightwaves.com/news/cass-the-freight-cycle-has-downshifted-with-a-thud

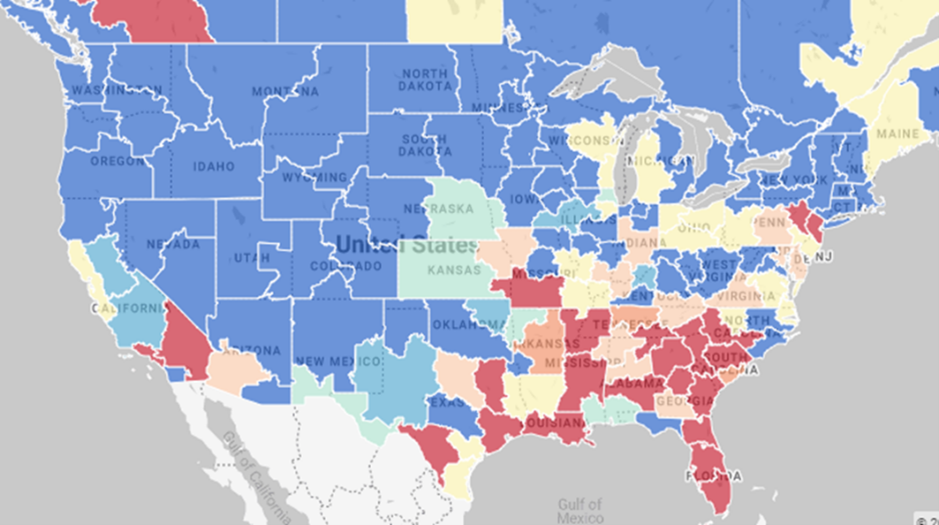

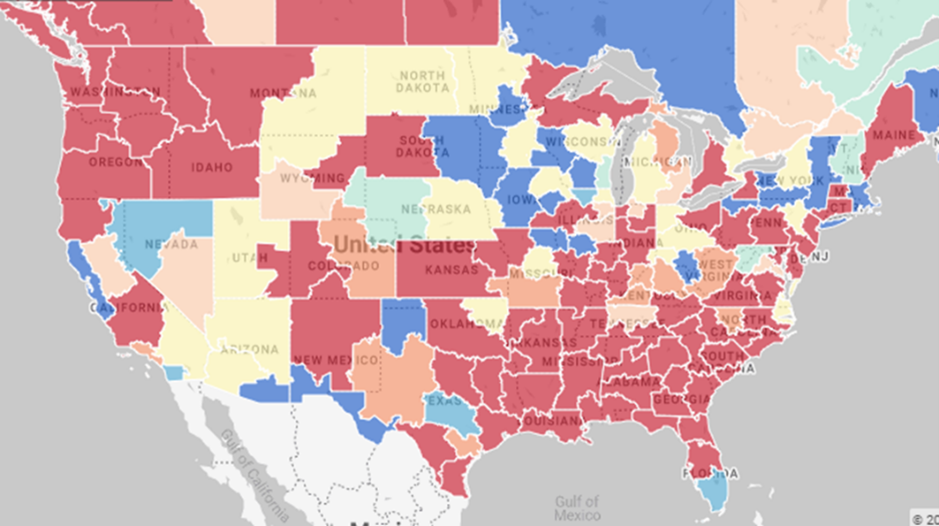

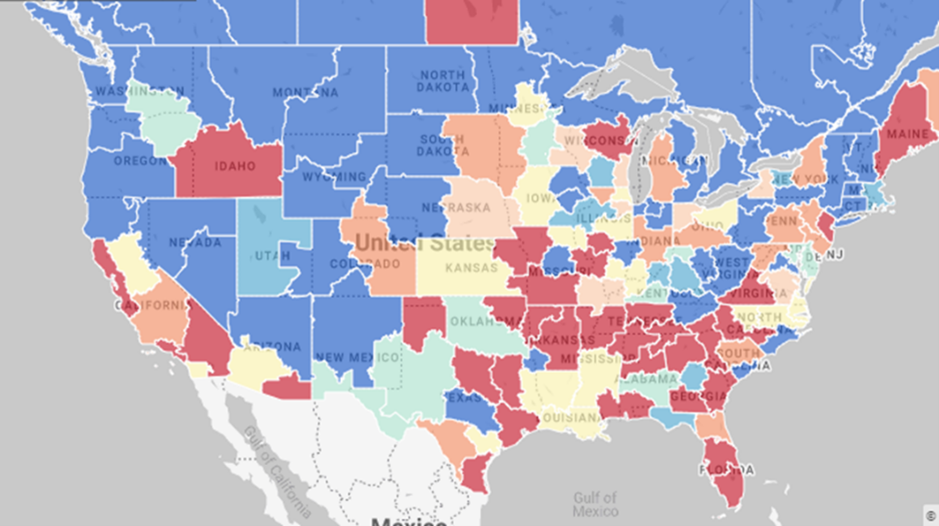

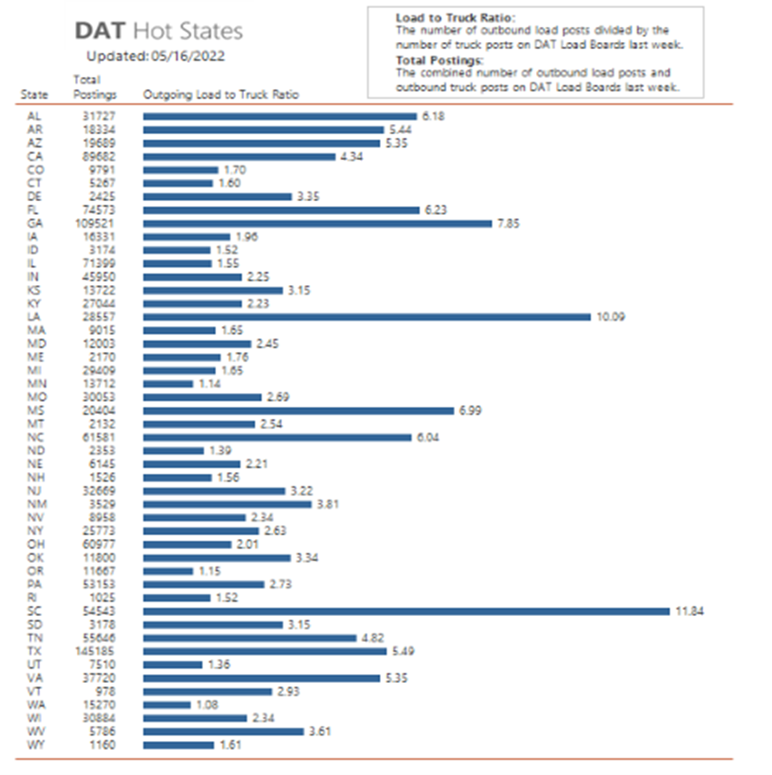

DAT Hot States: Vans, Flatbeds and Reefers

DAT Hot States for vans, flatbeds and reefers uses the MCI cool to hot, or -100 to +100, scale for measuring market temperature.

On the following U.S. maps, when the market is cool (darker blue areas), capacity is loose and in the negative range. When the market is hot (darker red areas), capacity is tight and in the positive range. The lighter colored areas (including yellow) capacity is more neutral.

Vans – May 2022

Flatbeds – May 2022

Reefers – April 2022

The load to truck ratio from DAT is a strong indicator of the balance between demand and capacity. Changes in the ratio could mean changes in rates. The higher the ratio, the tighter the capacity is for a particular state. As of May 16, 2022, DAT Hot States, the state with the highest load to truck ratio was South Carolina (11.84) with Washington (1.08) the lowest for the month.

Rate Outlook, Regulatory Update and Closing Thoughts

Shanghai Lockdown Reignites Supply-Chain Problems for U.S. Companies

Some U.S. companies are warning that Covid-19 lockdowns in Shanghai and elsewhere in China are denting sales, disrupting operations and putting added strain on supply chains that could be felt well into the summer.

Apple Inc. AAPL 4.10%▲ said it could take a sales hit of as much as $8 billion in its current quarter, primarily because of the Shanghai lockdowns. Industrial giant Honeywell International Inc. HON 4.47%▲ said the Covid measures had curbed production at half of its Chinese plants. J.B. Hunt Transport Services Inc. JBHT 3.32%▲ said the freight carrier’s customers are worried about deliveries scheduled for July.

Since the emergence of the virus, China generally has stuck to a zero-tolerance approach to dealing with flare-ups, using mass testing and travel restrictions along with widespread lockdowns. The latest wave in Shanghai started in early March, closing factories of companies including electric-car maker Tesla Inc. TSLA 4.77%▲ and consumer-products maker Procter & Gamble Co. PG 0.74%▲

Much of the rest of the developed world has adopted a strategy of minimizing Covid infections and managing waves while avoiding severe disruptions to business and daily life. Given China’s role as a key supplier to the world, the policy disparity has created an imbalance. Shanghai, a manufacturing and shipping hub of 25 million residents, accounted for 3.8% of China’s gross domestic product in 2021 and 7.2% of the country’s exports, according to Bank of America.

The Institute for Supply Management said its index of U.S. manufacturing activity in April hit its lowest level since July 2020, and the average time to receive production materials increased to 100 days in April, its longest span ever. In the survey, 15% of panelists expressed concern about the ability of partners in Asia to reliably make deliveries in the summer months, up from 5% in March.

Apple said it expects to lose $4 billion to $8 billion in sales during its fiscal third quarter ending in June because of its inability to meet customer demand, citing disruptions from Covid lockdowns and semiconductor shortages. The company said both problems are centered around the Shanghai corridor. Apple had $97.3 billion in second-quarter revenue.

Apple and other companies said they have restarted some operations that had been closed, as falling Covid case numbers have allowed more than half of the city’s residents to leave isolation.

Source for full article: https://www.wsj.com/articles/shanghai-lockdown-reignites-supply-chain-problems-for-u-s-companies-11651656601

The American Trucking Associations published a list of the products exempted under the pandemic-fueled relief. The three energy products – which ironically were added just as their peak winter usage season is ending – were listed along with gasoline, diesel, jet fuel and ethyl alcohol, which already were exempt.

The other areas exempted are:

- Livestock and livestock feed.

- Medical supplies connected to COVID-19 testing and treatment of procedures.

- Vaccines and supplies related to COVID-19 vaccination.

- Products related to community safety and sanitation for COVID-19, such as masks or gloves.

- Food and paper products to restock distribution centers or stores.

- An exemption for a broad category the ATA describes as “supplies to assist individuals impacted by the consequences of the COVID-10 pandemic.” It cites as an example building materials for people who have been displaced as a result of COVID-19.

ATA noted that the exemption will stay in effect until May 31 “unless extended by FMCSA.” Source for full article: https://www.freightwaves.com/news/fmcsa-adds-three-products-to-its-pandemic-waiver-which-faces-expiration-in-a-few-weeks

Closing Thoughts

Economy

Inflation, supply chain disruptions, continued COVID-19 impacts, and the labor shortages have many people fearful of an impending recession in 2022. These factors are putting pressure on many companies' margins. Companies are trying to not pass price hikes on to the customers because they know that increased cost will likely continue to push sales down. We continue to monitor how the transportation industry is responding to these issues.

Demand/Supply

As people begin to shift their spending habits from consumer products to cost of living due to inflation and higher gas prices, we are starting to see capacity in serval markets shift to benefit the shippers. The concern now is what is going to happen when the Chinese ports open back up. It is too early to tell if this is a sign of shipping trends returning to normal or just a pocket of relief. With produce season upon us, we will also potentially see things tighten slightly in the southeast areas.

We hope you enjoyed the latest GEODIS Industry Update digest and found it useful and informative. Please subscribe to receive future Industry Updates each month.

by

by