FEBRUARY 2022 GEODIS INDUSTRY UPDATE DIGEST

24/03/2022

24/03/2022Welcome to the February 2022 GEODIS Industry Update digest

Our monthly Industry Update provides the latest nationwide economic data, fuel-related concerns, modal rate outlooks, indexes as well as a variety of additional statistics and news items to provide a broad overview of what’s impacting the U.S. transportation industry nationally and globally.

Economic Overview

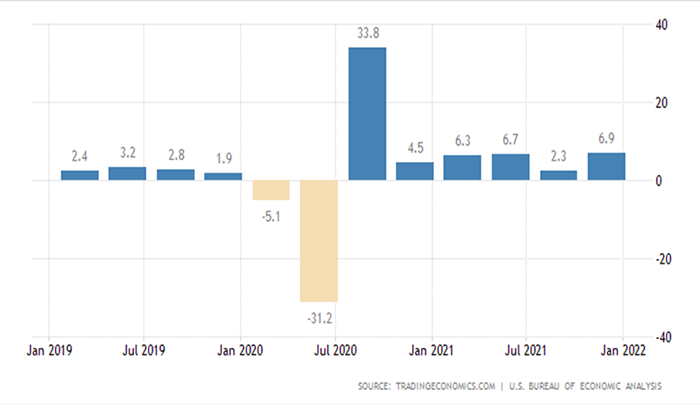

GDP

The American economy expanded an annualized 6.9% on quarter in Q4 2021, much higher than 2.3% in Q3 and well above forecasts of 5.5%. It is the strongest GDP growth in five quarters with the biggest upward contribution coming from private inventories (4.9 percentage points), namely motor vehicle dealers as companies that had been drawing down stocks since the beginning of 2021. Personal consumption increased 3.3%, pushed higher by a 4.7% surge in services spending, namely health care, recreation, and transportation.

U.S. Trade Deficit (December 2021)

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis reported that the goods and services deficit was $80.7 billion in December, up $1.4 billion from $79.3 billion in November, revised. December exports were $228.1 billion, $3.4 billion more than November exports. December imports were $308.9 billion, $4.8 billion more than November imports.

Unemployment Rate

The U.S. Bureau of Labor Statistics reported that nonfarm payroll employment rose by 199,000 in December, and the unemployment rate declined to 3.9 percent. Employment continued to trend up in leisure and hospitality, in professional and business services, in manufacturing, in construction, and in transportation and warehousing.

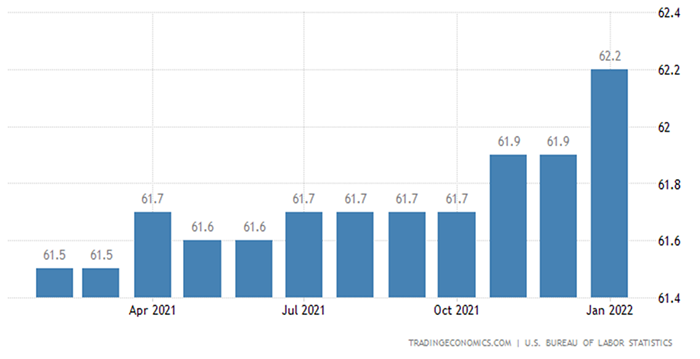

Labor Participation Rate

The labor force participation rate in the United States increased to 62.2 percent in January 2022, remaining still 1.2 percentage points lower than in February 2020 before the pandemic started.

Manufacturing

The ISM manufacturing index decreased by 1.2 points to 57.6 in January. Growth in new orders cooled a bit as did growth in production. The data suggests some supply chain improvements as the growth in backlogs slowed sharply. The pricing component rose. Industrial production declined 0.1% in December but rose 4.0% in the fourth quarter. Manufacturing fell 0.3% in December but rose 6.0% in the fourth quarter.

Consumer

Retail sales fell 1.9% in December but were 16.9% higher y/y. The decline was widespread. Automotive sales fell 0.4% from November but remained up 10.2% y/y. Furniture and home furnishing stores saw a 5.5% decline in December but were up 11.1% y/y. Non-store retailers saw an 8.7% decline in the last month of the year but remained up 10.7% y/y.

Residential Construction

New residential investment increased 1.4% in December to a seasonally adjusted annual pace of 1.502 million, the highest reading since March. The December increase was driven by the multi-family sector, which increased 13.7% to 524,000 units. Single-family starts fell 2.3% to 1.172 million. Total permits increased 9.1% to a 1.171 million annualized pace. Completions fell sharply, suggesting builders are struggling with supply chains and labor.

Fuel Forecasts and Trends

FTR Fuel Outlook

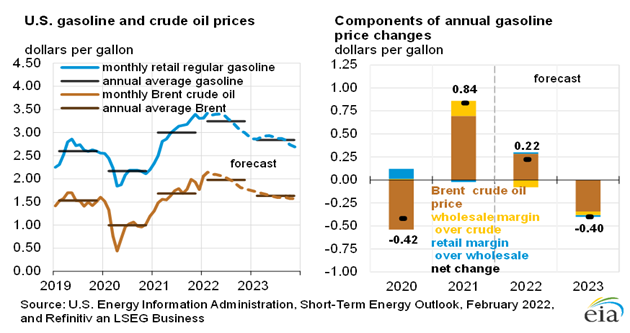

After steady declines throughout December, diesel prices soared more than 23 cents during January. The national average price of $3.846 per gallon is the highest since August 2014. Relief is unlikely soon. West Texas Intermediate on February 4 closed at $92.31 a barrel, which is the highest price since September 2014.

U.S. regular gasoline retail prices averaged $3.31 per gallon (gal) in January, unchanged from December 2021 and up 98 cents/gal from January 2021. Retail diesel prices averaged $3.72/gal in January, up 8 cents/gal from December and up $1.04/gal from last January. Product prices have risen compared with year-ago levels because of rising crude oil prices and high refining margins.

U.S. crude oil production reached almost 11.8 million b/d in November 2021 (the most recent monthly historical data point), the most in any month since April 2020. We forecast that production will rise to an average of 12.0 million b/d in 2022 and 12.6 million b/d in 2023.

Modal Update

Logistics News Flash:

Ukrainian conflict will lead to more supply chain woes

Russian import bookings declined 40% over the past week and will obviously fall further after growing ~64% in 2021 from the previous year, resulting in a 75% increase in goods by value, according to the Census Bureau. This put the imported goods value at its highest level since 2012. This direct economic hit will more than likely be dwarfed by the numerous indirect consequences of Russia’s recent invasion yet to come.

Many companies have realized that geopolitical risk has become one of the biggest threats to supply chain management over the past four years. The U.S. trade war with China highlighted how much our two economies are reliant on each other for success thanks to many American companies relying on cheaper foreign production of their goods.

Countries with autocratic leadership may have a low-cost labor force but our ideals are not in alignment, which increases the risk for confrontation. Russia is not America’s largest trade partner by a long shot — representing less than 1% of the total imports — but many of our largest trading partners, like Germany and China, have strong economic ties to the country.

Most of the current supply chain woes have been driven by demand that exceeds the current transportation capacity limits. This conflict will impact maritime shipping capacity worldwide and add to the already present price inflation.

Source for full article: https://www.freightwaves.com/news/ukrainian-conflict-will-lead-to-more-supply-chain-woes

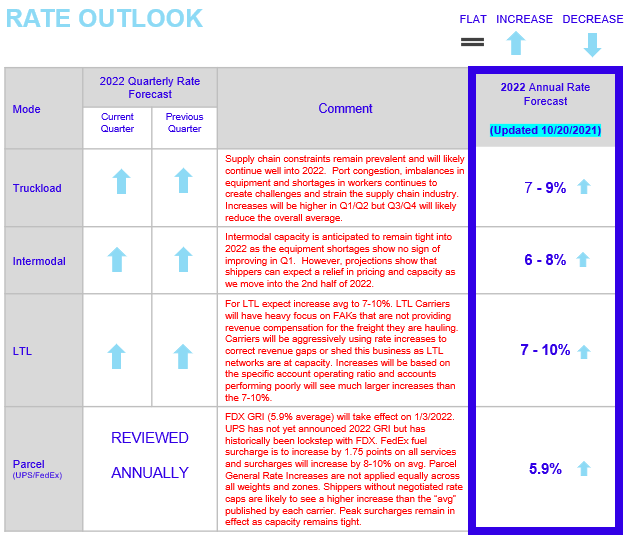

Rate Outlook Updates: Contract LTL, Truckload and Intermodal

The outlook for LTL rates is a half-point stronger at a 1.2% increase. The estimated 2021 gain was 17.4%.

FTR forecasts total truckload rates in 2022 at 2.4% higher y/y, excluding fuel, down from 2.7% previously.

Intermodal rate increases are expected to slim down over the course of 2022 before turning negative in the second half of the year. While rate increases are expected to turn negative for a time, it is worth noting that rates are at strong levels.

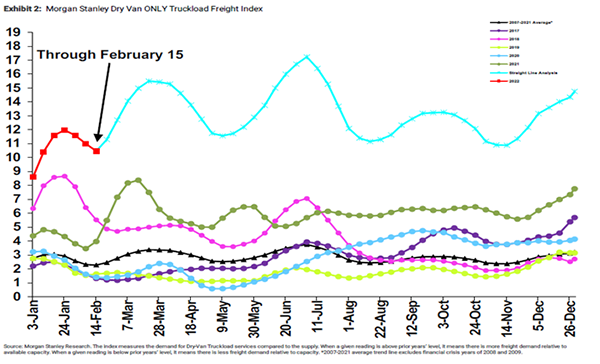

Morgan Stanley Index

The Morgan Stanley Index moves away from January’s all-time highs. After moving sideways last update, our TLFI followed typical seasonality and declined this update. However, supply and demand both underperformed as the underlying components missed typical seasonal trends by ~1,100 bps and ~300 bps respectively. Sequentially, the demand component declined by nearly 700 bps while the supply component increased by ~260 bps. Performance in our other indices was also mixed with our Flatbed index underperforming and remaining ~flat from our last update and our Reefer index outperforming seasonality despite declining sequentially.

Cass TL Linehaul Index (December 2021)

The Cass Truckload Linehaul Index® rose 2.2 points in January to 150.2 from 148.0 in December, up 1.5% m/m and up just 7.2% y/y, slower than the 8.0% increase in December. This data series trends below the ~20% increases in public TL fleet per-mile rates due in part to a large increase in length of haul (LOH) resulting from rail service issues pressing longer-haul shipments onto the highways. Accessorial fees (which our index does not include) are also part of the difference, but we estimate a 3% mix effect from longer LOH in January, which reduces the rate per mile even as cost per shipment rises.

Parcel Update:

Parcel shippers to feel more fuel surcharge pain

Time was that fuel surcharges were straight pass-through levies from the carriers to their customers. Surcharges accurately reflected a carrier’s fuel costs. Indices that set the surcharges were adjusted up or down depending on the direction of diesel and jet fuel prices.

Those days are long gone. Today, carriers routinely arbitrage fuel prices and surcharges to wring every revenue dollar out of their shipments. In the parcel-delivery sector, which is still dominated by FedEx Corp. (NYSE: FDX) and UPS Inc. (NYSE: UPS), there isn’t an attempt at subtlety. The two giants adjust their indexes whenever they want. They base their surcharges on diesel and jet fuel price bands of their own choosing. UPS has hiked its surcharge percentages three times since last August.

Users of UPS’ ground delivery and SurePost service in conjunction with the U.S. Postal Service currently pay a 12.75% fuel surcharge based on the nationwide on-highway diesel price of $4.03 a gallon set by the Department of Energy’s Energy Information Administration (EIA). The price is set each Monday, and the next adjustment will incorporate the impact of Russia’s invasion of Ukraine on fuel prices. UPS’ ground delivery surcharge will climb to 13% should diesel prices hit $4.10 a gallon or higher on Monday. Mike Erickson, president of AFMS LCC, a parcel consultancy, said he expects surcharge levels to “skyrocket” once the impact of the Russian invasion is reflected in Monday’s prices.

Small to midsize shippers have no recourse but to pay what the carriers demand. Bigger enterprise shippers must generate between $10 million and $20 million in shipping spend for either of the carriers to agree to negotiate fuel surcharge reductions.

Source for full article: https://www.freightwaves.com/news/parcel-shippers-to-feel-more-fuel-surcharge-pain

Current LTL Market:

Yellow adds driver schools, eyes training 1,000 drivers in 2022

Less-than-truckload carrier Yellow Corp. has announced the opening of two driver academies. The new schools are located in the transportation hubs of metro Atlanta and Cincinnati and are part of the carrier’s efforts to onboard new drivers to offset attrition during the year.

“We’re pleased to offer additional driver training locations,” Yellow CEO Darren Hawkins stated. “Our goal is to train 1,000 new drivers through our academies this year.”

The facilities complement 14 other Yellow (NASDAQ: YELL) owned and operated driver training centers around the country. The tuition-free centers provide in-class training and behind-the-wheel instruction. At the conclusion of the course, driver candidates will be ready for commercial driver’s license testing. Once the test is passed, trainees will complete a Department of Labor-certified apprenticeship with the company’s veteran drivers, eventually joining Yellow’s fleet as a professional driver.

The DOL apprenticeship provides pay in conjunction with on-the-job training. “Everything we teach emphasizes safety: safety of our drivers, colleagues, customers and the driving public, Hawkins added. “For anyone aspiring to a career that provides a good salary and full benefits that gets them on the open road and not behind a desk, trucking is a smart choice. Many of our drivers spend their entire careers with Yellow.”

Source for full article: https://www.freightwaves.com/news/yellow-adds-driver-schools-eyes-training-1000-drivers-in-2022

Hirschbach to Acquire John Christner Trucking

Hirschbach Motor Lines on Feb. 16 announced that it will acquire Sapulpa, Okla.-based refrigerated carrier John Christner Trucking.

Hirschbach, based in Dubuque, Iowa, is a privately owned carrier that provides refrigerated, dedicated and specialized transportation services. John Christner founded his namesake company in 1986, and later handed control over to his two sons, Danny and Darryl Christner.

Post-transaction, Danny will stay on as president while his brother and father plan to retire. John Christner Trucking will continue to operate as its own company, the companies said in a news release.

“These two organizations should be united and fit together like two puzzle pieces,” Hirschbach CEO Brad Pinchuk said in a statement provided to Transport Topics. “JCT covers the map coast-to-coast along the southern tier of the U.S. while Hirschbach’s density is largely east of the Rocky Mountains.”

Hirschbach will have more than 3,000 trucks when the deal closes, with 800 of them coming from JCT. The company also will have 5,000 trailers.

Source for full article: https://www.freightwaves.com/news/exclusive-christenson-transportation-acquires-family-owned-sharp

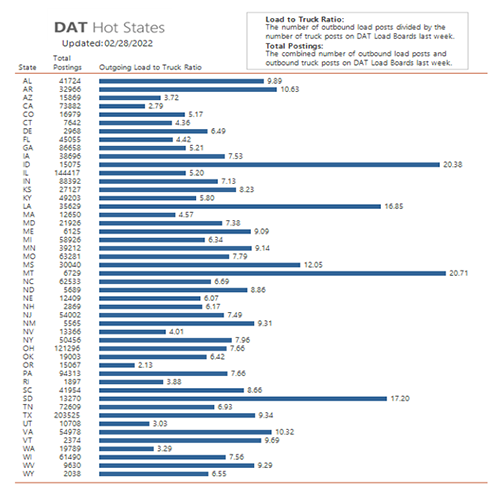

DAT Hot States: Vans, Flatbeds and Reefers

DAT Hot States for vans, flatbeds and reefers in January — using the MCI cool to hot, or -100 to +100, scale for measuring market temperature — is trending toward “hot” in all three sectors. When the market is cool, capacity is loose and in the negative range. When the market is hot, capacity is tight and in the positive range.

The load to truck ratio from DAT is a strong indicator of the balance between demand and capacity. Changes in the ratio could mean changes in rates. The higher the ratio, the tighter the capacity is for a particular state. As of February 28, 2022 DAT Hot States, the states with the highest load to truck ratios were Montana (20.71) and Idaho (20.38) with Oregon (2.13) the lowest for the month.

Rate Outlook and Regulatory Update

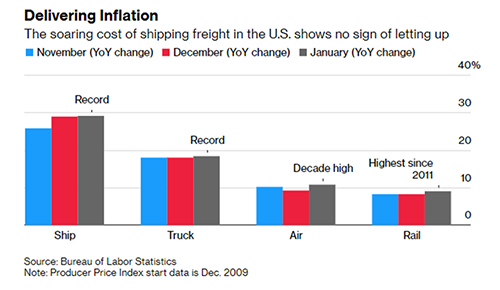

U.S. Freight Cost Blowout May Mean Little Inflation Relief Soon

Getting goods to market in the U.S. is becoming costlier by the month and that suggests American shoppers will find little relief from high inflation any time soon.

The costs of transportation and warehousing goods for final demand climbed another 1.4% in January from a month earlier, the government’s latest Producer Price Index showed. Compared with a year ago, the Labor Department’s gauge was up a whopping 16%, the largest annual advance in data back to 2009.

Looking across the various modes, the data showed an 18.3% jump in shipping by truck and a 29% surge in ocean freight costs from January of last year, the largest 12-month increases on record.

The cost of shipping by rail was up by the most since 2011 and air cargo inflation was the highest in a decade, according to the government’s detailed report on producer prices. What’s more, the prices of support services and warehousing have also soared. Arrangement of freight and cargo services cost a record 83.6% more in January than a year ago, while storage services were up an unprecedented 17.4%.

Shipping costs have become a bigger headache for companies such as Under Armour and Hasbro. Consumers, meanwhile, are already experiencing the worst inflation in four decades.

“The biggest challenge we have on the gross margin side right now is the freight costs,” David Bergman, Under Armour’s chief financial officer, said on the company’s Feb. 11 earnings call, adding that seaborne freight rates are “probably going to take a little bit longer to subside.”

Source for full article: https://www.bloomberg.com/news/newsletters/2022-02-16/supply-chain-latest-u-s-freight-cost-surge-means-little-inflation-relief

DOT to consider oral drug testing option for trucking

A new federal drug testing proposal aimed at saving the trucking industry time and money may prove less effective for cracking down on drivers who are habitual drug users, according to a regulatory expert.

The 120-page proposed rule from the U.S. Department of Transportation, scheduled for publication on Monday, would revise drug testing program procedures on the books since 1998 that require DOT-regulated industries to use only urine specimens for detecting drugs. Under the proposal, companies would be allowed to use oral fluid instead.

“The department believes that this proposed rule is needed because it makes several improvements in the integrity and effectiveness of an important safety program, as well as potentially reducing some costs to regulated parties,” DOT noted.

DOT listed several reasons for this belief, including enhanced flexibility, time and cost savings, and increased versatility in drug detection.

For example, giving employers the option of oral fluid testing provides them more flexibility in cases in which an employee is unable — for whatever reason — to provide a sufficient urine specimen. “The added flexibility will also benefit employees, who should be able to provide one of the specimen types, thereby facilitating the drug test required for their employment,” according to DOT.

Collecting an oral fluid sample can also require less time than collecting a urine sample, DOT points out, reducing time away from the workplace.

Source for full article: https://www.freightwaves.com/news/dot-to-consider-oral-drug-testing-option-for-trucking

Closing Thoughts: Economy and Demand/Supply

Economy

As the Omicron variant and inflation surges, household spending has continued to slow. The Federal Reserve stated that US industrial production fell for the first time since September as a result of the ongoing supply chain issues. Many shoppers heeded the warnings regarding shipping delays during the holiday season causing December spending to drop 8.7% from the October and November data. Experts are forecasting a strong rebound in sales once the Omicron variant surge subsides. However, as inflation rates continue to rise at a high speed, consumers are weary of spending beyond their comfort.

Demand/Supply

If you turn on the news, its rare to not hear a headline regarding the supply chain issues over the past year. From ships stuck at ports, warehouses overflowing, impactful shortages in drivers, empty shelves at the store, and out-of-stock messages online, 2021 was a disruptive year in a system that was already lean. Goods and services across the board have seen unprecedented shortages due to the pandemic’s ramifications and vulnerabilities. Since the Ford Assembly Line and the “Just in Time” Toyota methods were introduced to the world, manufacturing and production systems have been based on lean and efficient means. With COVID-19 boosting consumer demand in countless industries, it exposed the fragility of the situation.

We hope you enjoyed the latest GEODIS Industry Update digest and found it useful and informative. Please subscribe to receive future Industry Updates each month.

by

by