March Industry Update

24/03/2022

24/03/2022Welcome to the March 2022 GEODIS Industry Update digest

Our monthly Industry Update provides the latest nationwide economic data, fuel-related concerns, modal rate outlooks, indexes as well as a variety of additional statistics and news items to provide a broad overview of what’s impacting the U.S. transportation industry nationally and globally.

Economic Overview

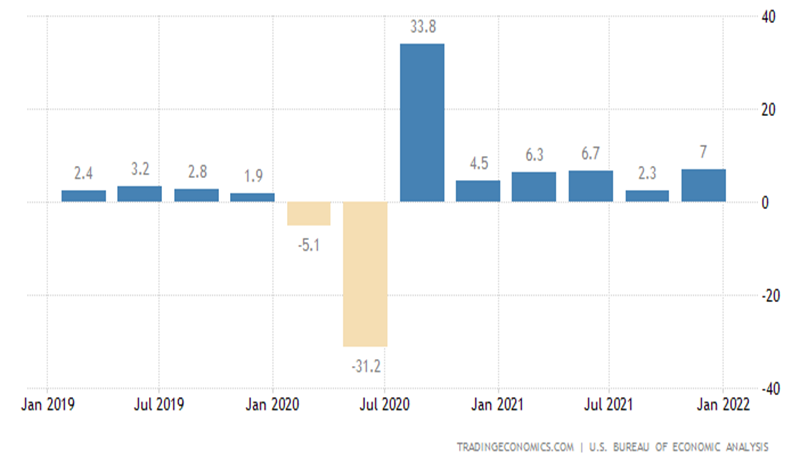

GDP

The American economy expanded an annualized 7% on quarter in Q4 2021, slightly higher than 6.9% in the advance estimate and in line with market forecasts. It remains the strongest expansion since a record growth of 33.8% in Q3 2020. The second GDP estimate showed a bigger rise in fixed investment (2.6% vs 1.3% in the advance estimate), mainly due to nonresidential one while residential fixed investment rebounded. On the other hand, both personal consumption (3.1% vs 3.3%) and exports (23.6% vs 24.5%) increased less than initially expected.

U.S. Trade Deficit (January 2022)

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis reports that the goods and services deficit was $89.7 billion in January, up $7.7 billion from $82.0 billion in December, revised. January exports were $224.4 billion, $3.9 billion less than December exports. January imports were $314.1 billion, $3.8 billion more than December imports.

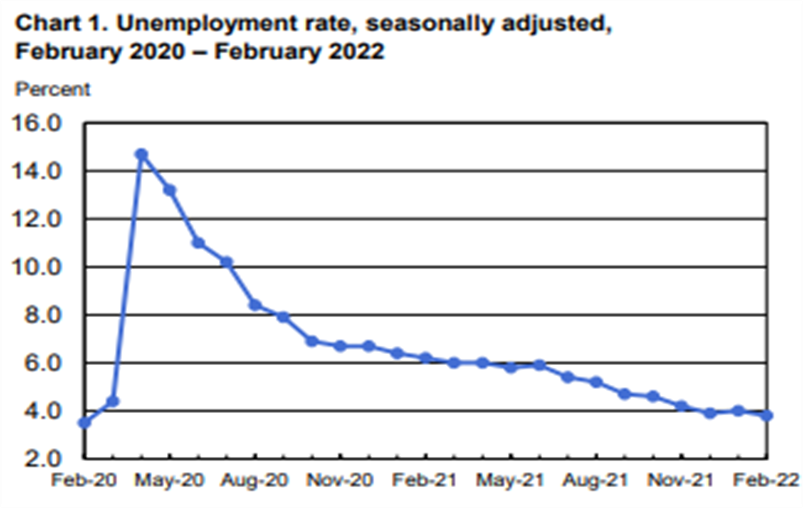

Unemployment Rate

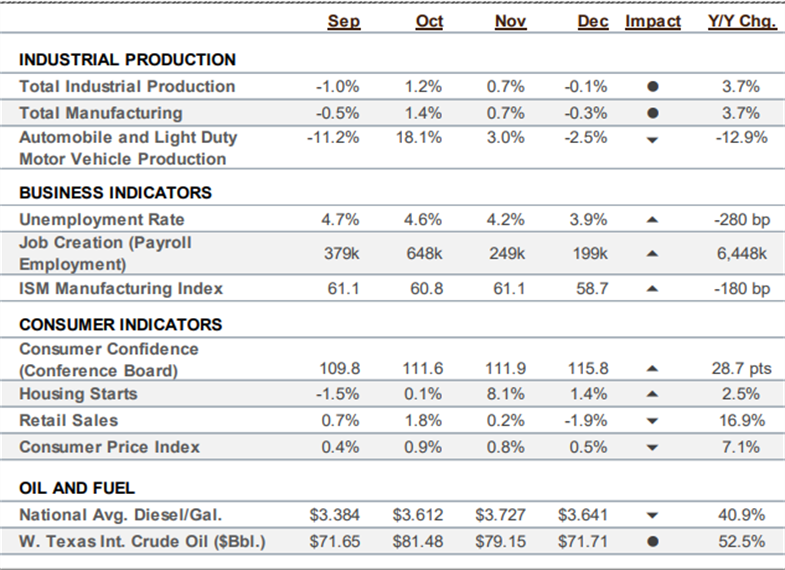

The U.S Bureau of Labor Statistics reports that nonfarm payroll employment rose by 678,000 in February, and the unemployment rate edged down to 3.8 percent, the U.S. Bureau of Labor Statistics reported today. Job growth was widespread, led by gains in leisure and hospitality, professional and business services, health care, and construction.

Labor Participation Rate

The labor force participation rate in the US edged up to 62.3 percent in February 2022, the highest level since March 2020.

Manufacturing

The ISM manufacturing index increased a point to 58.6 in February. After indications of supply chain challenges easing in January, the latest month showed new orders outpacing production and backlogs growing. In fact, acceleration of backlog growth represented the biggest change underlying the improvement in the ISM index. Industrial production increased 1.4% in January after a 1.0% decline in December. Manufacturing rose 0.2% during the month with modest gains in most sectors outside of automotive. The outlook looks good, and there are some signs of supply chain improvements.

Consumer

Retail sales rebounded sharply in January, but higher prices will blunt some of the impact on economic growth this quarter. Retail sales surged 3.8% in January, but data for December was revised down to a 2.5% decline. The January rebound was led by autos. Because of the supply situation, this year’s seasonal adjustment may have boosted the seasonal number slightly.

Residential Construction

New residential construction slowed in January as freezing weather hampered activity. Housing starts fell 4.1% in January to an annual rate of 1.638 million units. Single-family starts fell 5.6%. Freezing temperatures curtailed activity in the Northeast and Midwest. Total permits rose modestly by 0.7% to 1.899 million units.

Fuel Forecasts and Trends

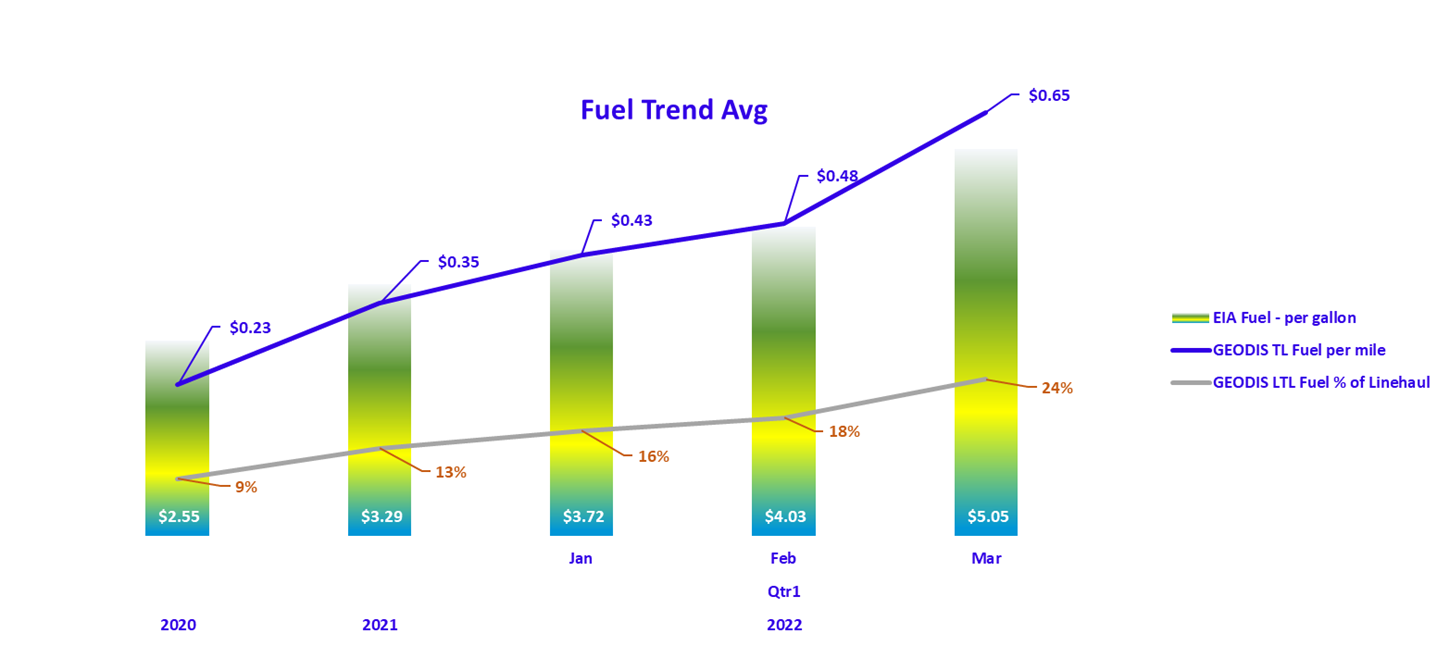

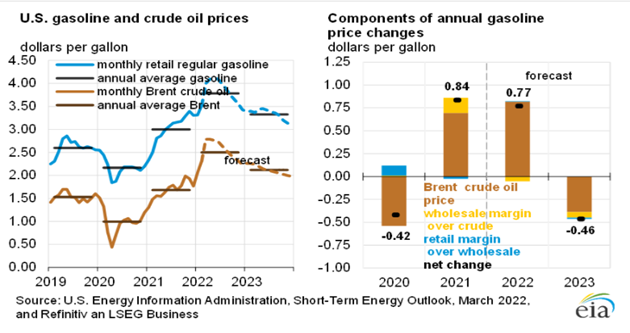

As fuel has continued to rise, the expense has become a larger percentage of the total cost of the shipment. Fuel has more than doubled throughout the country and analysts predict the prices to remain elevated for months to come. TL fuel has the potential to be 25% of the cost of the shipment if fuel hits $7.

Diesel prices ended February at the highest level in nine years, and further increases to the highest since August 2008 are certain due to surging crude prices in the wake of Russia’s invasion of the Ukraine. Diesel had already soared 49 cents in eight weeks. Crude closed above $100 a barrel on March 1 for the first time since July 2014.

U.S. regular gasoline retail prices averaged $3.52 per gallon (gal) in February, up 20 cents/gal from January and up $1.02/gal from February 2021. Retail diesel prices averaged $4.03/gal in February — the highest average price (not adjusted for inflation) for any month since March 2013. Product prices have risen compared with year-ago levels because of rising crude oil prices and high refining margins. We expect crude oil price increases will push the U.S. average gasoline price to $4.10/gal on average in 2022.

U.S. crude oil production fell below 11.6 million b/d in December 2021 (the most recent monthly historical data point), a decline of 0.2 million b/d from November 2021. We forecast that production will rise to average 12.0 million b/d in 2022 and then to record-high production on an annual-average basis of 13.0 million b/d in 2023.

Modal Update

Logistics News Flash:

White House Pushes Supply-Chain Operators to Share Data

The Biden administration launched a pilot program Tuesday to have ocean carriers, ports, trucks and major retailers share data with each other to improve the flow of goods through supply chains.

Transportation Secretary Pete Buttigieg, speaking at a White House roundtable with shipping-industry executives, said sharing information would help freight companies operate more efficiently and rein in the rising costs and extensive delays that have hampered U.S. supply chains over the past two years.

The initiative, called the Freight Logistics Optimization Works, is the latest effort by the White House to address bottlenecks that stretch from the country’s biggest gateway for overseas imports in Southern California to inland distribution hubs and warehouses. Goods often shift between various freight and logistics companies along the way to markets, and industry specialists say companies typically trade little information on shipments as they move. “Nobody can command this kind of sharing, but what we also know is that it needs to happen,” Mr. Buttigieg said.

The project will start out with 18 companies, among them, Target Corp., FedEx Corp., Switzerland-based Mediterranean Shipping Co., and freight middleman C.H. Robinson Worldwide Inc. The administration said it hopes to get the participation needed to build out the data exchange by the end of summer.

Source for full article: https://www.wsj.com/articles/white-house-pushes-supply-chain-operators-to-share-data-11647370851?mod=djemlogistics_h

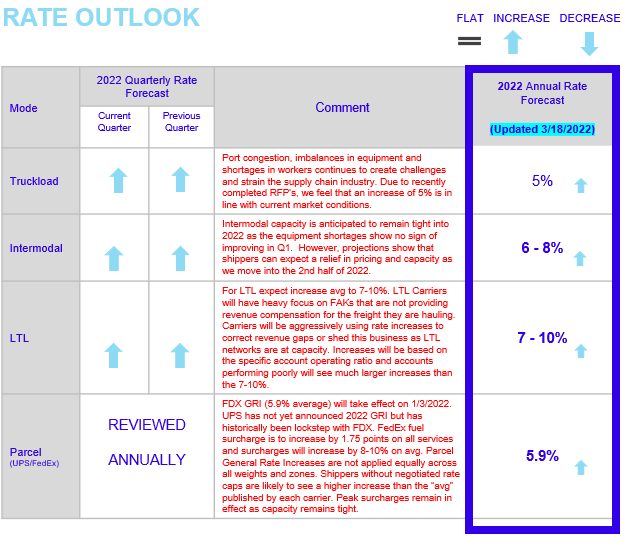

Rate Outlook Updates: Contract LTL, Truckload and Intermodal

The outlook for LTL rates is an increase of 2.4%, excluding fuel, on top of the 17.6% gain in 2021. The prior forecast was a 1.2% increase.

FTR forecasts truckload rate outlook for 2022 is stronger at an increase of 3.2% y/y, excluding fuel. Spot rates are now forecast to decline only 1.6% after a 29% surge in 2021. We expect contract rates to rise but not at the same levels as 2021. Depending on the freight profile a 6% - 8% increase is a realistic target for most businesses.

The intermodal rate outlook is little changed from last month. Rate increases will slowly ease over the course of 2022 before turning negative in the second half. We are seeing intermodal rates increasing and expect them to continue to do so unlike FTR is predicting. The strain of capacity and large providers switching railroad alliances has caused elevated rates which we do not think will drop until sometime in 2023.

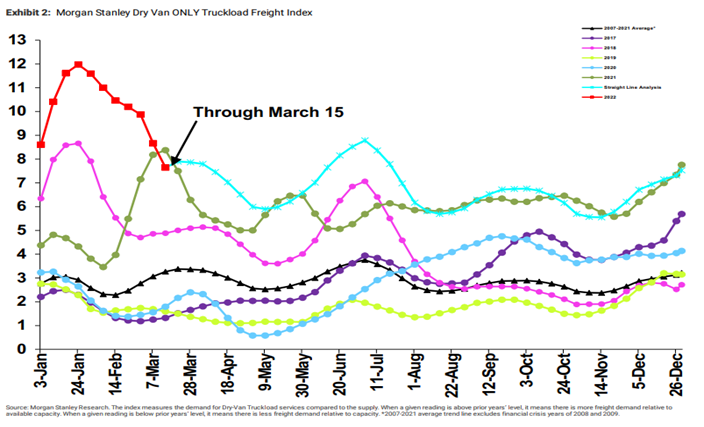

Morgan Stanley Index

TLFI underperforms seasonality significantly. Similar to the last update, our TLFI underperformed typical seasonality and declined sequentially. Both demand and supply underperformed as the underlying components missed typical seasonality trends by ~2,400 bps and ~1,600 bps respectively. Sequentially, the demand component declined by ~1,270 bps while the supply component increased by ~1,390 bps. Performance in our other indices was mixed with our Flatbed index increasing sequentially but under performing typical seasonality, while our Reefer index decreased sequentially and underperformed seasonality.

Cass TL Linehaul Index (December 2021)

The Cass Truckload Linehaul Index® rose 12.6% y/y in February after an upwardly revised 12.8% y/y increase in January to 158.0. Excess miles, rising fuel surcharges, and accessorial fees are all factors which are not reflected in the Cass Truckload Linehaul Index, so the increase in total truckload cost, depending on how these factors shake out, is between the 13% y/y increase in the Cass Truckload Linehaul Index and the 37% y/y increase in the inferred rate (which, as a reminder, is a mix of all domestic modes).

Parcel Update:

FedEx adds war surcharge as Ukraine crisis ratchets up shipping costs

FedEx Express notified customers on Thursday that it will hike its peak surcharge for many international parcel and freight shipments, beginning next week, because of the latest supply chain disruptions caused by the Russian invasion of Ukraine.

The express delivery company is increasing the surcharge by 20 to 30 cents per kilogram for most of Asia-Pacific, effective Monday, with price increases starting March 21 in other areas. European exports and imports are rising a tenth of a euro, or 11 cents, per kilogram. Increases also apply in the Indian subcontinent, Africa, and Latin America, according to the tariff schedule.

“Due to continued disruptions in the global supply chain, air cargo capacity remains limited. We are incurring incremental costs as we continue to adjust our international networks and operate in this constrained environment,” FedEx (NYSE: FDX) said a customer update.

The extra fee will also apply to shipments moving through FedEx’s intra-European network formerly known as TNT Express.

Memphis, Tennessee-based FedEx didn’t use the terms war surcharge or Ukraine, but news of the fee came nearly a week after the outbreak of hostilities roiled ocean, air and ground freight transportation in Europe and Russia.

Source for full article: https://www.freightwaves.com/news/fedex-adds-war-surcharge-as-ukraine-crisis-ratchets-up-shipping-costs

Current LTL Market:

Hot LTL market carries into 2022

Less-than-truckload carriers see strong demand trends from 2021 carry into what is normally the slowest part of the year. First-quarter updates from a couple of carriers Thursday highlighted robust revenue growth, driven by double-digit yield increases and higher volumes.

Old Dominion Freight Line (NASDAQ: ODFL) reported a 38.3% year-over-year increase in revenue during February, following a previously disclosed 25.7% increase in January. Tonnage jumped 18.3% in the month (+7.7% in January), with revenue per hundredweight, or yield, increasing16.8% in each of the first two months of the quarter.

The February comps benefited from severe winter storms during February 2021, which shut down portions of some carrier networks multiple times.

The growth trend was a little smoother on a two-year stacked comparison. Old Dominion’s revenue was 40.3% higher in January and up 47.5% in February when compared to 2020 levels. The two-year growth rates are attributed to nearly equal growth in tonnage and yields.

Worth noting, the 2022 yield metrics are being juiced by higher fuel surcharge revenue as diesel prices have soared again to start the year. On-highway diesel prices are up 38% year-over-year on average so far in 2022, reaching $4.10 per gallon in the latest week.

Old Dominion’s yield excluding the impact of fuel prices was 10.7% higher year-over-year for the first two months of the quarter, 610 basis points lower than the all-in growth rate.

The carrier said it continues to take share and will add the capacity needed to continue to do so. Old Dominion plans to open or expand eight to 10 terminals this year.

Source for full article: https://www.freightwaves.com/news/hot-ltl-market-carries-into-2022

Current Truckload Market:

XPO Logistics to Spin Off Freight Brokerage, Exit Intermodal and Europe Business

XPO Logistics Inc. plans to split its freight brokerage, European and intermodal businesses apart from its U.S. trucking operation, effectively dismantling the sprawling, multibillion-dollar freight and supply-chain operation that Chief Executive Brad Jacobs built through a decade of acquisitions.

The Greenwich, Conn.-based company, which spun off its contract logistics business last year as GXO Logistics Inc., said Tuesday it plans to separate its freight brokerage operation, which matches loads from shipping customers to available trucks, into a separate publicly traded company. XPO shareholders would hold shares in that separate business under what XPO said is intended to be a tax-free distribution.

The company, one of the largest logistics operators in North America, also plans to sell its North American intermodal business, which uses trucks and rail to move shipments, and to exit its European business through a sale or through a separate share listing in Europe.

XPO is currently under an exclusivity agreement to sell the intermodal business but declined to name the potential buyer.

“Our experience is that customers want high levels of service, and they want pure-plays, just as shareholders want pure-plays,” Mr. Jacobs said. Most of XPO’s investors, he said, “are highly focused on our LTL business and simply not giving us credit for our best-in-class truck brokerage business.”

The company expects the aggregate value of shares in the two newly split companies to exceed that of XPO’s stock if the companies remained combined. XPO’s shares currently trade at a “conglomerate discount,” Mr. Jacobs said.

XPO expects to complete the spinoff by the fourth quarter, subject to various requirements such as refinancing its debt with board approval.

Source for full article: https://www.wsj.com/articles/xpo-logistics-to-spin-off-freight-brokerage-11646773380

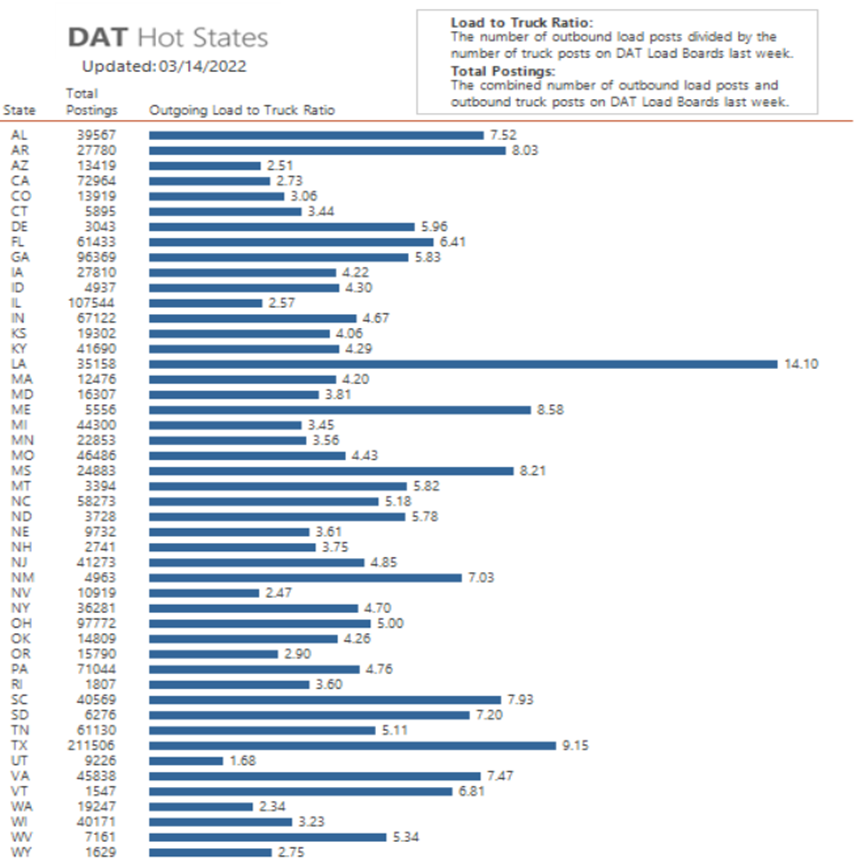

DAT Hot States: Vans, Flatbeds and Reefers

DAT Hot States for vans, flatbeds and reefers in March — using the MCI cool to hot, or -100 to +100, scale for measuring market temperature — is trending toward “hot” in all three sectors. When the market is cool, capacity is loose and in the negative range. When the market is hot, capacity is tight and in the positive range.

The load to truck ratio from DAT is a strong indicator of the balance between demand and capacity. Changes in the ratio could mean changes in rates. The higher the ratio, the tighter the capacity is for a particular state. As of March 14, 2022, DAT Hot States, the state with the highest load to truck ratio was Louisiana (14.10) with Utah (1.68) the lowest for the month.

Rate Outlook and Regulatory Update

Brokers Expect Rising Contract Rates for 2022

Freight brokerage firms are anticipating that contract rates will keep rising this year, with a slowdown not expected until year’s end.

“I think we’re going to definitely see continued strengths through the rest of the year, as capacity stays tight and as supply chains stay pretty messed up,” Evan Armstrong, president of the third-party logistics market research firm Armstrong & Associates, told Transport Topics. “The real key will be what happens going into 2023.”

Armstrong noted that while growth may slow headed into next year, factors that could maintain pressure on rates include diesel prices, robust consumer demand, international supply chain problems and the truck driver shortage. He suggested all of this will have an effect on companies’ margins.

“Operating costs and labor costs are going up,” Armstrong said. “The traditional gross margin of 15% now deteriorated to somewhere between 13% and 14% on truckload business.”

Bloomberg Intelligence and Truckstop.com released a survey Feb. 23 that found about 56% of brokers expect contract rates to rise over the next six months. About 75% expect factors such as restocking, increased economic activity, supply chain dislocations and driver availability will help propel growth.

“We’ve been in this bull market now for a little bit over 18 months,” Drew Herpich, chief commercial officer at Nolan Transportation Group, told TT. “I think the big question now is what happens to these contract rates going forward. During these situations, obviously, the assets really kind of drive this.”

In addition to the driver shortage, Herpich noted that insurance premiums are contributing to rate increases. He believes brokers will likely see rates increase in the high single digits to around 10% year-over-year.

Source for full article: https://www.ttnews.com/articles/brokers-expect-rising-contract-rates-2022

EPA Aims to Cut Toxic Emissions From Commercial Trucks

The Biden administration is proposing stricter rules to reduce air pollution from commercial trucks and buses, an effort it says will combat smog in major cities and the resulting respiratory problems.

The U.S. Environmental Protection Agency on Monday proposed new standards for engine manufacturers to lower nitrogen-oxide emissions from tractor-trailer-size trucks, as well as other delivery trucks, cement mixers and trash trucks.

The standards would take effect starting in model year 2027 and require manufacturers to create gasoline- and diesel-engine models with better exhaust systems. Industry officials say that could significantly raise the cost of new vehicles, which could lead older vehicles to stay on the roads longer — running counter to the administration’s public-health goals.

EPA officials said the proposed rules are ambitious but feasible and would benefit the public by reducing asthma and other health problems.

“These new standards will drastically cut dangerous pollution by harnessing recent advancements in vehicle technologies from across the trucking industry as it advances toward a zero-emissions transportation future,” EPA Administrator Michael Regan said.

The rules would reduce nitrogen-oxide emissions from the country’s fleet of heavy-duty trucks by as much as 60% in 2045, EPA officials said. Regulators last called on truck and engine manufacturers to reduce nitrogen-oxide gases from vehicle exhaust in 2001. Those regulations, which were fully phased in for vehicles made in model year 2010, prompted engine manufacturers to install devices that reduced emissions of the toxic gases that form when fuel is burned.

Source for full article: https://www.wsj.com/articles/epa-aims-to-cut-toxic-emissions-from-commercial-trucks-11646670626

Closing Thoughts: Economy Demand/Supply

Economy

The Bureau of Labor Statistics reports that the Consumer Price Index has double year over year. We can expect this increase to continue. As things in the Ukraine continue to heat up, we are starting to see the impact of the crisis here at home. We have seen record breaking fuel and transportation costs causing the price of everyday items to increase as well. The ever-increasing cost of goods has driven inflation to the highest it has been since 1982. Even though the unemployment rate continues to drop, inflation is still causing people to struggle to make ends meet. The fuel prices are also causing travel, that was expected to increase as many areas are lifting COVID mandates, to be limited.

Demand/Supply

We continue to see warehouses at capacity, extremely tight capacity markets and no shortage of demand for things. All sectors of the market seem to have a higher demand than the supply of that sector can support. It does not matter if you are talking about cars, houses, food or anything else for that matter.

We hope you enjoyed the latest GEODIS Industry Update digest and found it useful and informative. Please subscribe to receive future Industry Updates each month.

by

by